Complete Demat Account Guide India 2026 — What It Is, How It Works & Benefits

If you've ever wondered, "I want to invest in shares — but where do I even start?" — the answer is a demat account. It's your first step. Without it, you simply can't hold stocks, ETFs, or bonds in India. And yet, most beginners get confused before they even open one.

We've helped thousands of first-time investors at Finoda get this part right. So in this guide, we're walking you through everything — from what a demat account actually is, to how CDSL and NSDL work, to what charges you'll actually pay, and how to open one today.

No jargon. No fluff. Just the facts.

Quick answer: A demat account is a digital locker that holds your financial securities — stocks, mutual funds, bonds, ETFs — in electronic form. It replaced physical share certificates in India in 1996. You need it to invest in the Indian stock market.

→ Open Your Free Demat Account with Finoda

- What is a Demat Account? — Detailed Explanation

- Demat Account vs Trading Account — Key Differences

- CDSL vs NSDL — India's Two Depositories Explained

- How to Open a Demat Account Online — Complete Steps

- Demat Account Charges — AMC, DP Charges & Custodian Fees

- How Many Demat Accounts Can I Have?

- What Can You Hold in a Demat Account?

- Demat Account FAQs — All Questions Answered

- Ready to Open Your Demat Account?

What is a Demat Account? — Detailed Explanation

The word "demat" is short for dematerialised. Before 1996, investors in India received physical paper certificates when they bought shares. It was slow, risky, and frankly a nightmare to manage. Certificates got lost, forged, or damaged.

Then SEBI introduced dematerialisation. Shares moved from paper to an electronic format — and the demat account was born.

Think of a demat account like a bank account, but for your investments. Your savings bank account holds rupees. A demat account holds shares of Reliance, Tata, Infosys, or any company you invest in — digitally and securely. It also holds mutual fund units, government bonds, ETFs, sovereign gold bonds, and more.

So why does every investor need one?

Because you legally cannot hold or transfer shares in India without a demat account. It's not optional. Whether you're buying ₹500 worth of a mutual fund SIP or ₹50 lakh in a single stock, everything flows through your demat account.

In our experience at Finoda, most beginners assume the demat account is the same as the trading account or the bank account. It isn't. Each plays a different role — and we'll cover that next.

Want to understand how stock markets work first? Read our Stock Market Basics Hub.

Demat Account vs Trading Account — Key Differences

Here's where people get genuinely confused. And honestly, the confusion is understandable — brokers often open both together.

A demat account stores your securities. That's its only job. It holds them, keeps them safe, and lets you check your portfolio anytime. Think of it as a cupboard.

A trading account is what you use to buy and sell those securities. It's the buying/selling interface — connected to NSE and BSE. Think of it as the door to the market.

And your bank account is where money moves in and out. It funds your trades and receives your sale proceeds.

All three work together. But they're not the same thing. When you buy shares of any company:

- Money leaves your bank account

- The trade executes through your trading account

- Shares land in your demat account

When you sell, it works in reverse.

Most brokers — including the platforms we work with at Finoda — open all three accounts together as a package. But it's important you understand what each does. Otherwise, when something goes wrong (and occasionally, something does), you won't know where to look.

Planning to trade actively? See our guide on Intraday Trading and understand the risks before you start.

CDSL vs NSDL — India's Two Depositories Explained

When you open a demat account, your securities don't actually sit with your broker. They sit with one of two government-registered depositories — CDSL (Central Depository Services Limited) or NSDL (National Securities Depository Limited).

Both are regulated under the Depositories Act, 1996. Both are safe. Your broker acts as a Depository Participant (DP) — a middleman between you and the depository.

NSDL was India's first depository, launched in 1996. It's backed by NSE, IDBI Bank, and UTI Bank, among others. Historically, NSDL held more institutional accounts and was linked to earlier brokerage platforms. It uses a 16-digit account number format.

CDSL was launched in 1999, promoted by BSE. It's now the larger of the two depositories by number of demat accounts, having crossed 13 crore registered accounts in 2024. CDSL uses a 16-digit numeric BO ID.

So which is better? Honestly, for most retail investors, it doesn't matter. What matters more is the quality of your broker/DP. Both depositories are equally safe, regulated, and reliable. Your broker will assign you to one of them automatically.

One practical difference: CDSL's EASI and Easiest portals let you view and track holdings directly online. NSDL has its own SPEED-e and IDeAS portals for the same purpose.

Check the official SEBI website for depository regulations and investor rights.

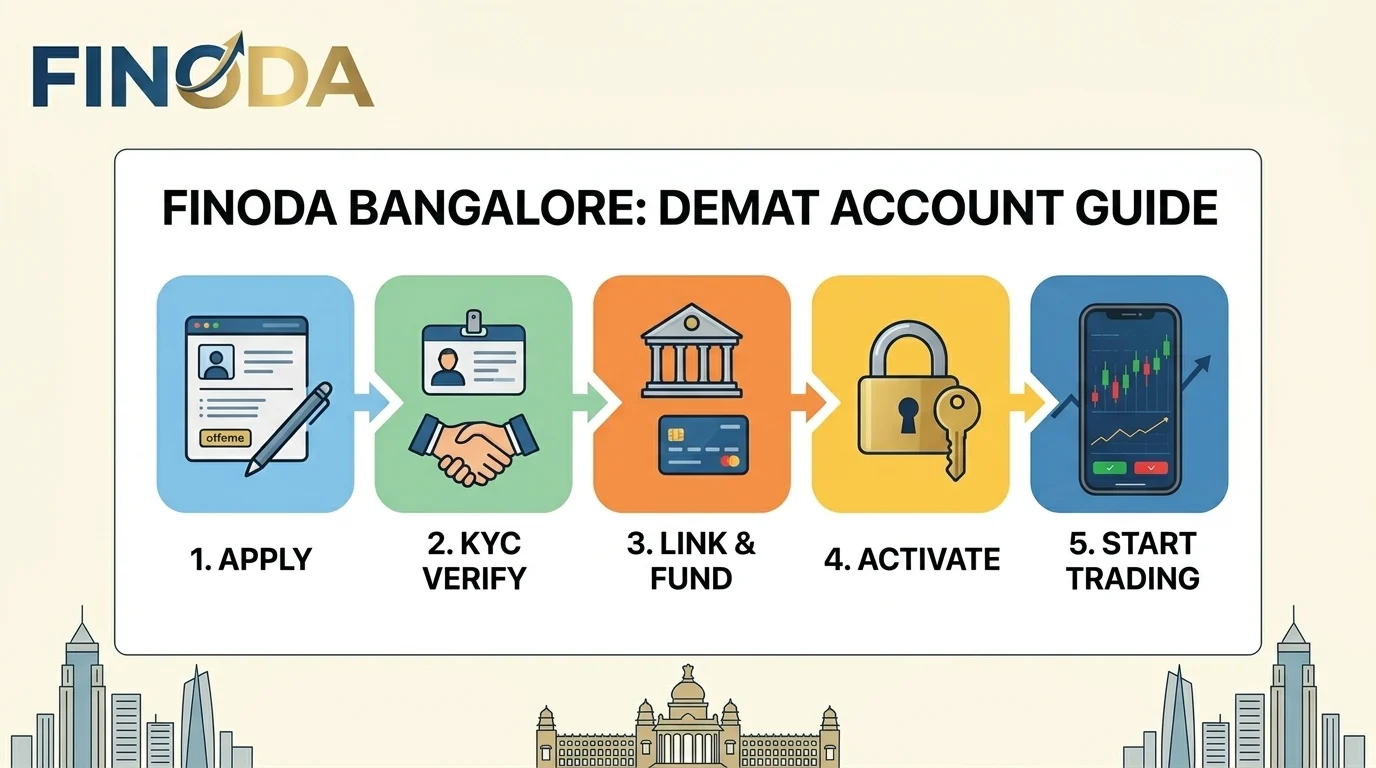

How to Open a Demat Account Online — Complete Steps

Good news: opening a demat account today takes less than 30 minutes. Most of it is digital. You don't need to visit any office — everything happens online through eKYC.

Here's the step-by-step process:

Step 1 — Choose a Depository Participant (DP)

Your DP is the broker or institution through which you open the account. At Finoda, we guide you through the entire process and help you pick the right platform based on your investment goals — whether it's long-term wealth, IPO investing, or active trading.

Step 2 — Collect Your Documents

You'll need:

- PAN card (mandatory — and it must be linked to Aadhaar)

- Aadhaar card (for eKYC verification)

- Bank account details — a cancelled cheque or recent bank statement

- Passport-size photograph

- Signature (scanned or live during video KYC)

Important: As of 2025, SEBI mandates that your PAN and Aadhaar must be linked. If they aren't linked, your application will be rejected. Check your PAN-Aadhaar link status here before applying.

Step 3 — Fill the Online Application

Visit your chosen broker's website or app. Fill in your basic details — name, address, PAN, bank info. At this stage, you'll also choose whether you want a standalone demat account or a demat + trading account combo. We always recommend the combo for anyone who wants to actively buy or sell.

Step 4 — Complete eKYC and Video Verification

SEBI requires In-Person Verification (IPV). But don't worry — this is a short video call. You'll show your PAN card on camera, confirm your name, and speak a displayed code. The whole thing takes about 5 minutes.

Step 5 — e-Sign and Submit

Once verified, you'll e-sign the documents using your Aadhaar OTP. No printing, no courier, no physical signatures. Just an OTP to your registered mobile.

Step 6 — Receive Account Credentials

After internal verification (typically 24–48 hours), you'll receive:

- Your BO ID (Beneficiary Owner ID — your unique demat account number)

- Login credentials for your trading platform

- A welcome kit with your account details

That's it. You're ready to invest.

→ Open Your Demat Account with Finoda Today

Already have a demat account? Start your investment journey with our SIP Investment guide or explore IPO Investing.

Demat Account Charges — AMC, DP Charges & Custodian Fees

One of the most common questions we hear is: "Is there any hidden charge?" Fair question. So let's break down every possible charge you might encounter.

1. Account Opening Charge: Many brokers now offer free account opening. Some charge a one-time fee of ₹200–₹500.

2. Annual Maintenance Charge (AMC): This is a yearly fee for maintaining your demat account. It typically ranges from ₹0 to ₹750 per year depending on your broker. Some brokers offer the first year free. After that, charges kick in.

3. Transaction / DP Charges: Every time you sell shares from your demat account, a DP (Depository Participant) charge applies. This is usually ₹10–₹25 per debit transaction, regardless of trade size.

4. Custodian Fees: Some brokers charge a small fee for holding certain securities — especially for institutional clients. For most retail investors, this isn't applicable.

5. Pledge and Unpledge Charges: If you pledge your shares as margin for trading, brokers may charge ₹30–₹60 per pledge/unpledge request.

Note: Demat accounts don't charge you for buying. Charges typically come when you sell. Also, your trading brokerage is separate from demat charges.

We'd strongly recommend reading the full charge structure of any platform before opening an account. At Finoda, we walk every client through this transparently — no surprises.

Understand how to maximise returns on your investments. Read our Long-term Investing guide.

How Many Demat Accounts Can I Have?

Yes, you can have more than one demat account in India. There's no legal restriction on the number. You can open accounts with multiple DPs using the same PAN card.

But should you? That's a different question.

Multiple demat accounts make sense if you actively trade on one platform while keeping long-term holdings on another, or if you want to compare broker platforms before committing. However, each account comes with its own AMC and fees. Plus, managing multiple portfolios adds complexity — especially at tax time when you need to compute capital gains across accounts.

In our experience at Finoda, most retail investors do just fine with one well-chosen demat account. If you're unsure which platform suits your goals, talk to us — we'll help you decide without any sales pressure.

Learn about Equity Trading and Derivatives — F&O to understand what your demat account enables you to do.

What Can You Hold in a Demat Account?

More than most people realise. Here's a quick list:

- Equity shares — Listed company stocks on NSE/BSE

- Bonds & NCDs — Government securities and corporate bonds

- Mutual fund units — Including ELSS funds

- ETFs — Exchange-Traded Funds

- Sovereign Gold Bonds (SGBs) — RBI-issued gold bonds

- IPO allotments — Shares credited directly after allotment

- REITs and InvITs — Real estate and infrastructure investment trusts

- Insurance policies (in electronic form through demat)

So a demat account isn't just for stocks. It's your complete investment storage system.

Interested in SGBs or bonds? Read our Fixed Deposit Investment and Mutual Funds guides to compare options.

Demat Account FAQs — All Questions Answered

Frequently Asked Questions About Demat Accounts in India

A demat account is a digital account that holds your financial securities — shares, bonds, mutual funds, ETFs — in electronic form. You need it because Indian stock exchanges (NSE and BSE) don't allow physical share transfers. Every buy or sell transaction requires a demat account by law.

No. They're different. A demat account stores your securities. A trading account is what you use to place buy/sell orders on the stock exchange. Most brokers open both together, but they serve distinct functions.

With eKYC, the process takes about 15–30 minutes. Account activation typically happens within 24–48 hours after your documents are verified and IPV is completed.

You need: PAN card, Aadhaar card (linked to PAN), a bank document (cancelled cheque or statement), a passport-size photo, and a scanned signature. Your PAN and Aadhaar must be linked — otherwise your application will be rejected.

Technically yes — you can open a standalone demat account. But without a linked trading account, you can't buy or sell securities. For practical investing, you need both.

Your securities in a demat account are held by CDSL or NSDL — not by your broker. Even if your broker shuts down, your holdings remain safe with the depository. This is a critical safety feature of the Indian demat system.

BO ID stands for Beneficiary Owner Identification. It's your unique 16-digit demat account number. You'll need it when applying for IPOs, transferring shares, or logging into CDSL/NSDL portals.

AMC stands for Annual Maintenance Charge. It's the yearly fee your broker charges to maintain your demat account. It ranges from ₹0 to ₹750 depending on the broker and plan you choose.

Yes. You can open multiple demat accounts with different brokers using the same PAN. However, each carries its own charges. Most investors find one account sufficient.

Both are SEBI-regulated depositories that hold your securities electronically. NSDL was India's first, launched in 1996. CDSL was launched in 1999 and is now larger by account count. For retail investors, both are equally reliable. Your broker decides which one you're registered with.

Yes. You can submit a demat account closure request to your DP. But first, all holdings must be transferred out or sold. Closing an unused account avoids unnecessary AMC charges.

No. A demat account has no minimum balance requirement. You can even hold a zero-balance demat account — though you'll still be charged AMC by your broker.

Yes. NRIs can open NRE-linked or NRO-linked demat accounts depending on whether they're investing using foreign or domestic income. Different rules and RBI permissions apply for each type.

Your demat account can be transferred to a nominee. This is why adding a nominee during account opening is strongly recommended. The nominee needs to submit certain documents to claim the holdings.

Log in to your broker's platform or directly to the CDSL EASI portal or NSDL IDeAS portal using your BO ID. You can view all holdings, transactions, and statements online at any time.

→ Still have questions? Talk to our team at Finoda — we're happy to help.

Ready to Open Your Demat Account?

We've covered a lot. But here's the simple truth: a demat account is not complicated. The paperwork takes less than half an hour. The whole thing is digital. And once it's open, you've unlocked access to every stock, ETF, bond, IPO, and mutual fund in India.

At Finoda, we don't just help you open an account — we help you understand what to do next. Whether you're starting with a ₹500 SIP or planning a ₹5 lakh equity portfolio, our team in Bangalore is here to guide you through every step.

→ Open Your Free Demat Account Now

Or call us at +91 90352 94343 | Email: info@finoda.in

Related Guides You'll Find Useful

- Stock Market Basics Hub — Start from the very beginning

- Mutual Funds Guide — The easiest way to get started

- SIP vs Lumpsum — Which suits you better?

- IPO Investing — How to apply for IPOs with your demat account

- ELSS Funds Guide — Save tax and grow wealth

- Financial Planning Guide — Build a plan before you invest

- Tax-Saving Investments — Make your demat account work smarter

- Glossary of Financial Terms — Decode every financial term

Content written by the Finoda team, Bangalore. All investments are subject to market risks. Please read all scheme-related documents carefully before investing. Finoda operates within SEBI guidelines.