Invest in Mutual Funds India 2026 — Expert-Guided Selection

A mutual fund pools money from thousands of investors and puts it to work across stocks, bonds, and other assets — all managed by a professional fund manager. You don't need to pick individual stocks. You don't need a crore in savings. And you don't need to sit glued to market charts.

What you do need is the right fund for your goal — and that's exactly where we come in.

At Finoda, we're AMFI-registered mutual fund advisors based in Bangalore. We've helped 10,000+ investors across Karnataka find funds that actually match their timelines, tax situations, and comfort with risk. Our operations follow SEBI guidelines, so every recommendation we make is grounded in regulatory compliance and transparency.

📞 Book a Free Consultation →What is a Mutual Fund? — A Beginner-Friendly Explanation

Think of it this way. You and 999 other people each put ₹10,000 into a shared pool. That pool — worth ₹1 crore — is handed to a professional fund manager who invests it across 30–50 companies. Any gains or losses are shared proportionally. That's a mutual fund.

In India, all mutual funds work under SEBI's regulatory framework and are distributed through AMFI-registered advisors. The Association of Mutual Funds in India (AMFI) sets the code of conduct for all fund distributors — including us.

So when you invest through Finoda, you're not buying a product from us directly. Your money goes straight into the fund, held by the fund house (AMC). We're here to guide which fund, how much, and when.

Why are mutual funds popular in 2026? The Indian mutual fund industry crossed ₹72.20 trillion in AUM as of May 2026 — nearly three times what it was just five years ago. SIP inflows hit record highs in early 2026. Clearly, more and more people have started trusting this route for building wealth. And honestly, it makes sense.

Types of Mutual Funds in India — Choose What's Right for You

Not all mutual funds are the same. In our experience, most confusion among new investors comes from not knowing which type of fund to start with. So let's break this down simply.

Equity Mutual Funds — For Long-Term Wealth Creation

Equity funds invest primarily in company stocks. They carry higher short-term risk, but historically they've delivered the best long-term returns among all fund categories.

Within equity funds, you'll encounter three sub-categories. Large-cap funds invest in the top 100 companies by market cap — think stable, reliable names. Mid-cap funds target companies ranked 101–250, offering more growth potential but slightly more volatility. And small-cap funds go further down the list — higher risk, but the returns over a 7–10 year horizon can be significantly higher.

If you're in your 20s or 30s, or you have a goal that's at least 5 years away, equity funds deserve serious consideration. We'd suggest starting with a diversified flexi-cap or large-cap fund if you're new to this.

Debt Mutual Funds — For Safety and Regular Income

Debt funds invest in government bonds, corporate bonds, and money market instruments. They're not technically "safe" in the sense that returns are guaranteed — but they carry far less volatility than equity funds.

If you have money you might need within 1–3 years, or if you're nearing retirement and want to preserve what you've built, debt or liquid funds are worth looking at. Liquid funds in particular are excellent alternatives to keeping money idle in a savings account — they're highly liquid and generally offer better post-tax returns than FD for short durations.

ELSS Funds — Tax Saving + Wealth Creation

ELSS (Equity Linked Savings Scheme) is one of the smartest instruments under Section 80C. You can claim a deduction of up to ₹1.5 lakh per year, and the lock-in is only 3 years — the shortest among all 80C options. Plus, since ELSS invests in equities, the growth potential is much higher than PPF or NSC over the long term.

We've found that ELSS works best as part of a broader tax-planning strategy, not just as a standalone fund. Combine it with NPS contributions and you've got a fairly efficient tax structure.

Index Funds — Low-Cost Market Returns

Index funds simply mirror a benchmark index — like Nifty 50 or Sensex. They don't try to beat the market; they track it. As a result, their expense ratios are very low (often under 0.20%), and there's no dependency on a fund manager's judgment.

In 2026, index funds have seen massive inflows from first-time investors and those switching from traditional savings instruments. If you want simplicity and cost-efficiency, a Nifty 50 index fund is hard to argue against as a core holding.

Hybrid Funds — Balanced Growth & Safety

Hybrid funds invest in both equity and debt — in varying proportions depending on the fund type. Aggressive hybrid funds might hold 65–80% in equities. Conservative hybrid funds lean more toward debt. Balanced advantage funds dynamically shift allocation based on market valuations.

For investors who aren't comfortable going all-in on equities but still want inflation-beating returns, hybrid funds are a solid middle ground. We often recommend these for medium-term goals in the 3–5 year range.

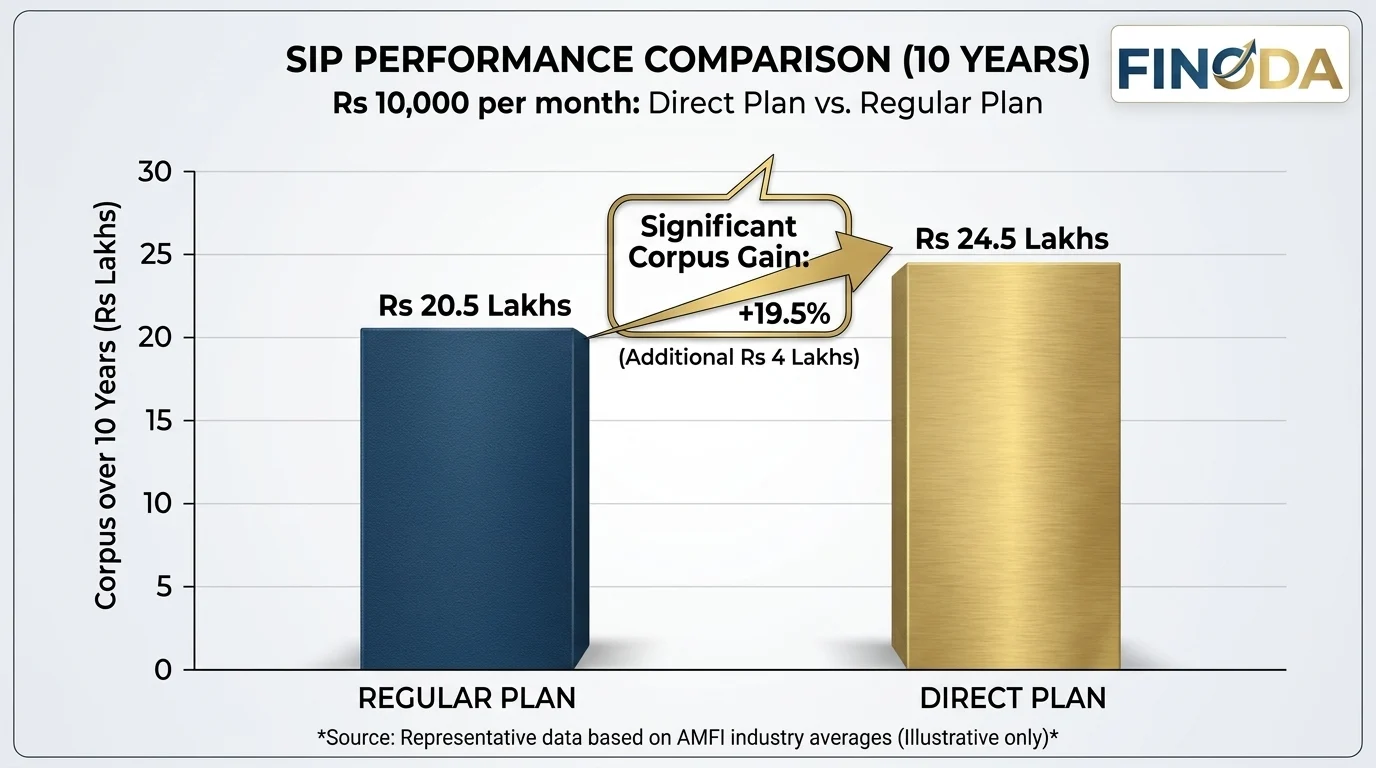

Direct Plan vs Regular Plan — Which Should You Choose?

Direct vs Regular mutual fund — which gives higher returns over time?

Direct vs Regular mutual fund — which gives higher returns over time?

This is one of the most Googled questions in mutual fund investing — and for good reason.

Direct plans don't involve a distributor. You invest directly through the AMC or a platform. Because there's no advisor commission, the expense ratio is lower, which means slightly better returns over time.

Regular plans route your investment through an AMFI-registered advisor like Finoda. Yes, there's a small advisory cost built into the expense ratio. But here's what that buys you: someone who knows your complete financial picture, reminds you not to panic during market corrections, reviews your portfolio every quarter, and helps you rebalance when needed.

The data does show that direct plans deliver marginally higher returns. But the same data also shows that most direct plan investors end up switching funds at the wrong time, missing SIPs during market dips, or staying in under-performing funds because no one flagged it. In our experience, the value of good advice routinely exceeds the cost of that advice.

That said — the choice is yours. If you're financially literate, disciplined, and happy to do your own research, direct works fine. If you want a partner in this, regular through Finoda makes more sense.

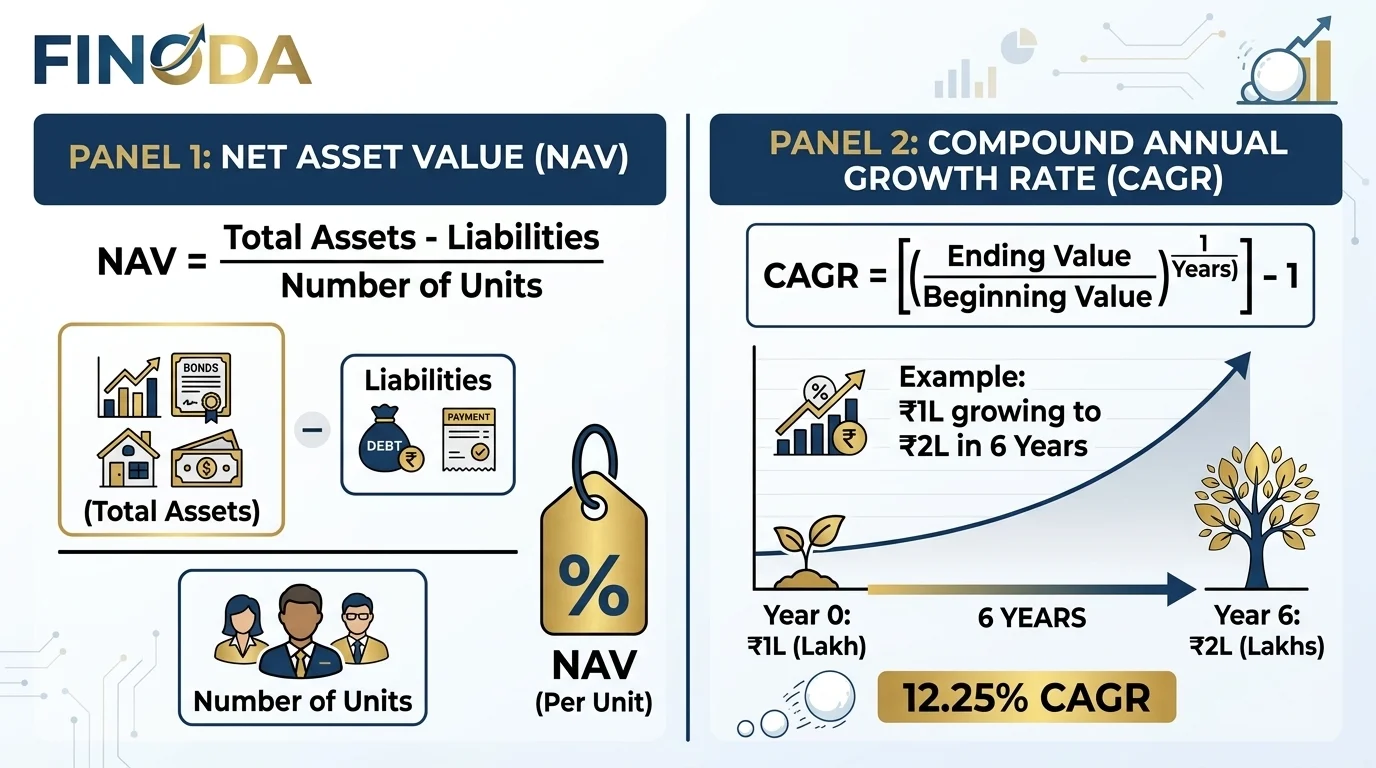

How Mutual Fund Returns Are Calculated — NAV & CAGR Explained

How NAV and CAGR work in mutual funds — a simple visual explainer

How NAV and CAGR work in mutual funds — a simple visual explainer

Two terms you'll see everywhere in mutual fund discussions are NAV and CAGR. Both are important. Neither is complicated.

NAV stands for Net Asset Value. It's the price at which you buy or sell one unit of a mutual fund. It's calculated every business day as:

A higher NAV doesn't mean a fund is expensive. It just means the fund has been around longer or has grown more. Comparing NAVs across funds to decide which is "cheaper" is a common mistake — avoid it.

CAGR stands for Compound Annual Growth Rate. It tells you the smoothed annual growth rate of your investment over a period. If you invested ₹1 lakh and it grew to ₹2 lakh in 6 years, the CAGR is approximately 12.25%.

Why does CAGR matter? Because point-to-point returns can be misleading. A fund that grew 80% in one year and fell 20% the next looks great on an absolute basis but not so great on a CAGR basis. Always compare mutual funds using CAGR over 3, 5, and 10 year windows — and cross-check against category averages on Value Research.

Also note: past performance is not a guarantee of future returns. This isn't just a legal disclaimer — it's genuinely important to internalize.

How to Invest in Mutual Funds with Finoda — Step by Step

Personalized mutual fund advice from Finoda's AMFI-certified advisor — Bangalore

Personalized mutual fund advice from Finoda's AMFI-certified advisor — Bangalore

Investing in mutual funds through Finoda is straightforward. Here's exactly how it works.

Step 1 — Book a Free Consultation

Call us on 9035294343 or fill out our contact form. We'll schedule a no-obligation 30-minute call to understand your goals, income, existing investments, and time horizon.

Step 2 — Risk Profiling

We use a structured questionnaire to determine where you sit on the risk spectrum — conservative, moderate, or aggressive. This directly informs which fund categories suit you best.

Step 3 — Fund Selection

Based on your profile and goals, we present a curated shortlist of 3–5 funds. We explain the rationale behind each — the fund manager's track record, category performance, expense ratio, and how it fits into your overall portfolio.

Step 4 — KYC and Account Setup

First-time investors need to complete KYC (Know Your Customer) — a one-time process done online. We walk you through this. If you already have a Demat account through Finoda, this step is even faster.

Step 5 — SIP or Lumpsum — Your Choice

You decide how much and how often. SIP is the go-to approach for most salaried investors — it automates investing and removes the temptation to time the market. Lumpsum works well for windfall amounts or bonuses.

Step 6 — Quarterly Reviews

We don't just set it and forget it. Every quarter, we review your portfolio against your goals and current market conditions. If a fund consistently underperforms its category benchmark, we flag it.

Are You Using Mutual Funds for Tax Saving?

Most investors don't realize that ELSS mutual funds give you the best combination of tax savings and wealth creation available under Section 80C. Deduction up to ₹1.5 lakh. Three-year lock-in. Equity growth. Compare that to PPF (15-year lock-in) or NSC (fixed returns), and ELSS looks very attractive for anyone with a medium-to-long investment horizon.

And it doesn't stop there. If you're also saving for retirement, an NPS Investment → gives you an additional ₹50,000 deduction under Section 80CCD(1B) — something not many people know about. Between ELSS and NPS, you can build a remarkably efficient tax strategy.

Need full tax planning? Check our Tax Advisory Hub → or explore Income Tax Filing → for end-to-end compliance support.

Why Investors in Bangalore Choose Finoda for Mutual Funds

We're not the cheapest option on the market. We're also not the flashiest. But we've found that what most investors actually want — especially after their first bad experience with a pushy broker — is someone who gives a straight answer.

Here's what working with Finoda actually looks like:

- No product pushing. We recommend funds based on your goal, not on what gives us the highest commission.

- AMFI-registered. Every recommendation we make complies with AMFI's code of conduct and operates within SEBI's regulatory framework.

- Real advisors, not bots. You speak to a real person. Questions get answered the same day, not buried in a ticket queue.

- One relationship, everything covered. From mutual funds to insurance, loans, NPS, and equity trading — you don't need four different providers anymore.

- 8+ years in Bangalore markets. We know the local investor mindset. We know the questions that don't make it onto FAQ pages.

We're in Kodihalli, Bangalore — VGV Towers, Unit 101, HAL Old Airport Road, near Leela Palace. Walk in if you'd prefer a face-to-face conversation.

Quick Comparison — Which Mutual Fund Type Suits You?

| Fund Type | Risk Level | Ideal For | Time Horizon | Tax Benefit |

|---|---|---|---|---|

| Large-Cap Equity | Moderate | Steady long-term growth | 5+ years | No |

| Mid/Small-Cap | High | Aggressive growth | 7–10 years | No |

| ELSS | Moderate-High | Tax saving + wealth | 3+ years (lock-in) | 80C up to ₹1.5L |

| Index Fund | Low-Moderate | Low-cost market returns | 5+ years | No |

| Hybrid | Moderate | Balanced growth-safety | 3–5 years | No |

| Debt/Liquid | Low | Capital preservation, short goals | Under 3 years | No |

Frequently Asked Questions — Mutual Funds India

A mutual fund pools money from many investors and invests it in a diversified portfolio of stocks, bonds, or other securities, managed by a professional fund manager. In India, mutual funds are regulated by SEBI and distributed through AMFI-registered advisors.

Yes — and no, depending on which fund you pick. Mutual funds are market-linked, so they carry varying levels of risk. Equity funds have higher risk with higher return potential; debt funds are lower risk. Diversification within funds reduces single-stock exposure significantly. But no mutual fund guarantees returns — and past performance is not indicative of future results.

Direct plans skip the distributor, giving a slightly lower expense ratio and marginally better returns. Regular plans include an advisor fee — but come with expert guidance, quarterly reviews, and ongoing support. For most investors who aren't fully self-sufficient in fund research, the guidance in a regular plan genuinely adds value beyond the cost.

NAV (Net Asset Value) is the per-unit price of a mutual fund, calculated daily as: (Total Assets − Liabilities) ÷ Total Units. You buy and sell mutual fund units at the prevailing NAV. A lower NAV doesn't mean a fund is cheaper or better — it simply reflects its history.

You can start a SIP from as little as ₹100–₹500 per month. For lumpsum investments, most funds require a minimum of ₹500–₹1,000. There's no upper limit. Our SIP Calculator can help you figure out how much monthly investment is needed to reach a specific goal.

For beginners, large-cap equity funds or hybrid funds are a practical starting point — they offer less volatility than mid or small-cap funds. Nifty 50 index funds are also popular: low cost, simple, and broadly diversified. We'd recommend starting your journey with our Mutual Funds Guide.

ELSS (Equity Linked Savings Scheme) qualifies for a deduction of up to ₹1.5 lakh per year under Section 80C of the Income Tax Act. It has a 3-year lock-in — the shortest among all 80C instruments — and it invests in equities, so the long-term growth potential is significantly higher than traditional tax-saving instruments like NSC or PPF.

Yes. You can pledge mutual fund units as collateral and get a Loan Against Securities. This means you don't have to redeem your investments when you need urgent funds. Your investment stays in the market, continues to grow, and you repay the loan separately. Finoda facilitates this through our Loan Against Securities service.

A SIP (Systematic Investment Plan) lets you invest a fixed amount every month automatically. Lumpsum means a one-time large investment. SIPs benefit from rupee-cost averaging — you automatically buy more units when markets are low, fewer when high. Lumpsum works better when you have a large corpus and markets are at a low point. Not sure which to choose? Read our SIP vs Lumpsum guide.

For equity mutual funds, short-term capital gains (held under 1 year) are taxed at 20%. Long-term capital gains (held over 1 year) above ₹1.25 lakh are taxed at 12.5%. For debt funds bought after April 2023, all gains are now added to your income and taxed at your slab rate. ELSS follows equity taxation rules. For detailed guidance, see our Income Tax Filing page.

The expense ratio is the annual fee a mutual fund charges to manage your money, expressed as a percentage of AUM. SEBI reduced maximum expense ratios by up to 15bps in 2026, making mutual fund investing more cost-efficient. Index funds typically charge under 0.20%; active equity funds range from 0.50% to 1.0–2.1% depending on AUM slab. Over 10–20 years, even a 0.50% difference in expense ratio meaningfully impacts your final corpus.

The right fund depends on your goal (wealth creation, tax saving, capital preservation), time horizon, and risk tolerance. Short goals under 3 years suit debt or liquid funds. Medium-term goals of 3–5 years suit hybrid funds. Long-term goals of 5+ years suit equity funds. The honest answer, though, is that a 20-minute call with one of our advisors will tell you more than any checklist. Book your free consultation →

Ready to Start Investing in Mutual Funds?

The industry has crossed ₹72 trillion. Monthly SIP flows are at all-time highs. And India's mutual fund market is projected to reach ₹100 lakh crore by 2030. The people building real wealth through mutual funds aren't the ones who found the perfect fund — they're the ones who started and stayed consistent.

You don't need to get it perfect on day one. You need to get started.

Call us on 9035294343 or write to info@finoda.in. Or just stop by at our office — VGV Towers, Unit 101, 100 Feet Ring Rd, Jayanagara 9th Block, Bengaluru 560041. No appointment needed for a quick chat.

📞 Book a Free Consultation → Open Demat Account → Try SIP Calculator →