SIP vs Lumpsum Investment India 2026 — Which is Better for You?

Every month, more than 9.79 crore Indians invest through SIPs. And yet, the question "SIP or lumpsum — which is better?" still confuses a lot of people. We don't blame you. Both routes have real merit. Both have genuine risks. And neither is universally "right."

In our experience at Finoda, the answer almost always depends on your situation — your income, your savings, your goals, and honestly, how you'd feel watching your investment drop 20% overnight. This guide cuts through the noise and gives you a straight answer.

Open a Free Demat Account with Finoda →

Table of Contents

- What is SIP Investing? — Quick Recap

- What is Lumpsum Investing? — One-Time Investment Explained

- SIP vs Lumpsum — Head-to-Head Comparison Table

- When SIP Wins Over Lumpsum

- When Lumpsum Wins Over SIP

- Expert Verdict — SIP or Lumpsum for Indian Investors?

- Frequently Asked Questions — SIP vs Lumpsum

- Related Reading from Finoda's Education Hub

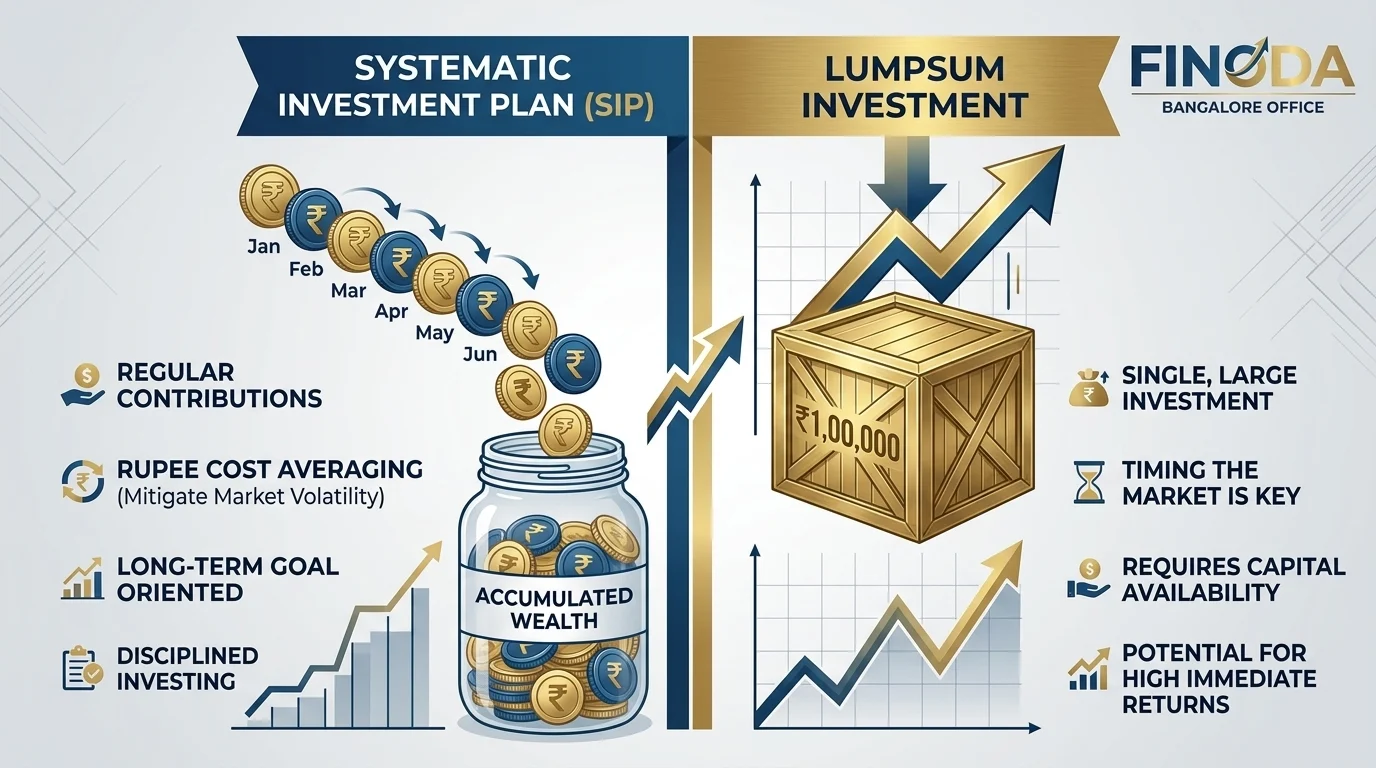

What is SIP Investing? — Quick Recap

A Systematic Investment Plan — or SIP — lets you invest a fixed amount into a mutual fund every month. Think of it like an EMI, but instead of paying off a loan, you're building wealth.

You can start with as little as ₹500 a month. Some platforms even allow ₹100. The money gets auto-debited from your bank and units of the chosen mutual fund get credited to your folio. Simple.

The real power of SIP lies in something called rupee cost averaging. When markets fall, your ₹500 buys more units. When markets rise, it buys fewer. Over time, this averaging effect pulls down your overall cost per unit — and that's where the magic happens for long-term investors.

There's also the Step-Up SIP option, where you increase your monthly amount by a fixed percentage every year. If you get a salary hike, your SIP can grow with you. This is one of the most underused features in Indian mutual fund investing.

In December 2025, India's total SIP inflows crossed ₹31,000 crore in a single month — a new all-time high. That's not a coincidence. Millions of Indians have figured out that SIP is the quietest, most effective path to building serious wealth over time.

Internal Links:

External Link: AMFI India — Official SIP Data

What is Lumpsum Investing? — One-Time Investment Explained

Lumpsum is exactly what it sounds like — you invest one large amount at once. No monthly commitments. No auto-debits. You put in the full corpus on day one, and from that moment, every rupee is working in the market.

The minimum for most equity mutual funds in India is ₹5,000. After that, additional investments can often be made in multiples of ₹1,000 or ₹500, depending on the fund house.

Lumpsum investing works brilliantly when you catch the market at a low point. If you had invested ₹6 lakh in a flexi-cap fund during the March 2020 COVID crash, you'd be looking at extraordinary returns today. That's the upside. But timing the market perfectly is genuinely difficult — even for professionals.

So where does lumpsum make sense? When you've received a windfall — a bonus, a property sale, an inheritance — and you want to put that money to work immediately. Also, if you're an experienced investor who understands market cycles and can sit calmly through a 30% drawdown, lumpsum might be the right tool.

But if you're a first-time investor or someone who'd lose sleep watching the market drop — lumpsum can be emotionally brutal.

Internal Links:

SIP vs Lumpsum — Head-to-Head Comparison Table

| Feature | SIP | Lumpsum |

|---|---|---|

| Investment Style | Fixed amount at regular intervals | One-time, large investment |

| Minimum Amount | ₹100–₹500/month | ₹1,000–₹5,000 (one-time) |

| Market Timing Risk | Low — spread across time | High — timing-dependent |

| Rupee Cost Averaging | ✅ Yes | ❌ No |

| Suitable For | Salaried, first-time investors | Experienced, windfall investors |

| Compounding Benefit | Gradual, over years | Immediate on full corpus |

| Flexibility | Start/pause/modify anytime | One-shot decision |

| Emotional Ease | High — disciplined & automatic | Lower — needs nerves of steel |

| Best Market Condition | Volatile or sideways markets | Bull markets, market corrections |

| Returns Potential | Steady, consistent | Higher peak returns possible |

The numbers back this up too. Analysis of Nifty 50-based funds over different market cycles shows that SIPs delivered more stable returns during volatile periods, while lumpsum outperformed during sustained bull runs. Both are valid. Neither is wrong.

When SIP Wins Over Lumpsum

SIP isn't just "safe" — it's smart in the right conditions. And in our experience, those conditions apply to most Indian investors most of the time.

SIP is the better choice when:

You have a monthly salary and want to build wealth steadily. You don't have a large lump of cash available right now. Markets are at high valuations and a correction feels possible. You're new to investing and still learning. You want to invest for a long-term goal like retirement, a child's education, or a home. Volatility makes you anxious — and you know that anxiety leads to bad decisions.

The rupee cost averaging benefit is real. When the Nifty fell in 2022, SIP investors who stayed put bought units at lower prices. When the market recovered, their portfolios bounced back faster than people who tried to "wait for the bottom" before making a lumpsum investment.

Step-Up SIP is worth a special mention here. If you increase your SIP amount by 10–15% every year — in line with your salary growth — the difference in your final corpus over 20 years is staggering. We've found that investors who use Step-Up SIP consistently build meaningfully more wealth than those who set a fixed SIP and forget it.

When Lumpsum Wins Over SIP

Lumpsum isn't the enemy. In fact, there are times when deploying a large amount upfront is clearly the smarter move.

Lumpsum makes more sense when:

Markets have just corrected significantly and valuations look attractive. You've received a one-time windfall — bonus, inheritance, property sale proceeds. You're investing in a debt fund or liquid fund (low volatility, lumpsum is perfectly fine here). You have a very long time horizon of 10+ years and can hold through multiple market cycles. You're an experienced investor who has been through at least one full market cycle without panicking.

The data supports this. Over extended bull runs — like 2010–2015 and the post-COVID recovery of 2020–2021 — lumpsum investors often generated higher absolute returns than SIP investors putting in the same total amount. The full corpus benefits from market gains from day one.

But here's the catch: you rarely know in advance whether you're at the start of a bull run or a bear market. That uncertainty is exactly what makes lumpsum risky for most people.

One strategy we often discuss with our clients: if you have a large amount to invest, consider a hybrid approach. Deploy 60–70% via SIP over 12–18 months through a Systematic Transfer Plan (STP), and keep the rest in a liquid fund. It gives you some lumpsum advantage while managing downside risk.

Expert Verdict — SIP or Lumpsum for Indian Investors?

Here's our honest take.

For most Indians — particularly those with a regular salary, first-time investors, or anyone who hasn't been through a full market crash yet — SIP is the better starting point. It removes the anxiety of timing. It enforces discipline. And it builds real wealth over time without requiring you to watch the Nifty every morning.

But "SIP vs lumpsum" shouldn't be a permanent either/or decision. We've found that the best investor portfolios often combine both. A core SIP running month after month, with occasional lumpsum top-ups during sharp market corrections.

The worst thing an investor can do? Nothing. Waiting for the "perfect time" to invest is how people miss years of compounding. Markets will always feel risky. That's the price of growth.

We operate within SEBI guidelines to ensure every recommendation at Finoda is transparent, fair, and in your best interest. Whether you're starting with ₹1,000/month or deploying ₹10 lakh as a lumpsum — we help you find the right path.

Internal Links:

Open your free demat account with Finoda in minutes and begin your SIP today.

Open Free Demat Account →Frequently Asked Questions — SIP vs Lumpsum

Q1. What is the main difference between SIP and lumpsum investment?

SIP means you invest a fixed amount every month into a mutual fund — like ₹1,000 or ₹5,000. Lumpsum means you put a large amount in at one go. SIP spreads your investment over time, which reduces the risk of market timing. Lumpsum puts your full corpus to work immediately, which is great in a rising market but risky if the market falls right after you invest.

Q2. Is SIP better than lumpsum for long-term investing?

For most investors in India — especially salaried individuals — SIP is generally better for long-term wealth building. It enforces discipline, benefits from rupee cost averaging, and removes the pressure of timing the market. However, if you receive a windfall and invest it during a market correction, lumpsum can generate stronger returns. The best approach is often a combination of both.

Q3. Can I do both SIP and lumpsum at the same time?

Yes, absolutely. Many experienced investors use a hybrid strategy — running a regular SIP for consistent wealth building while making occasional lumpsum investments during market dips. This gives you the best of both worlds: discipline from SIP and opportunistic returns from lumpsum.

Q4. What is Step-Up SIP and should I use it?

Step-Up SIP (also called Top-Up SIP) allows you to increase your monthly SIP amount by a fixed percentage every year. For example, if you start with ₹5,000/month and increase it by 10% annually, your SIP grows alongside your income. Over 20 years, the difference in your final corpus is substantial compared to a fixed SIP. We strongly recommend it to anyone with growing income.

Q5. Which is better for a market correction — SIP or lumpsum?

Both can work during corrections, but in different ways. A lumpsum investment during a sharp correction can deliver excellent returns if you have the conviction to hold long-term. However, if you're not sure about the timing, a SIP — or an STP (Systematic Transfer Plan) from a liquid fund — is a safer way to deploy funds during uncertain markets.

Q6. What is the minimum amount to start a SIP in India?

You can start a SIP with as little as ₹100 per month on some platforms. Most equity mutual funds in India accept ₹500/month as the standard minimum. Some funds require ₹1,000/month. At Finoda, we can help you find funds that match your budget and goals.

Q7. What is the minimum amount for lumpsum investment in India?

For most equity and hybrid mutual funds in India, the minimum lumpsum amount is ₹5,000 for a first-time investment. Some fund houses allow ₹1,000. Additional lumpsum investments in an existing folio can often be made in multiples of ₹500 or ₹1,000.

Q8. Does SIP guarantee returns?

No. SIP does not guarantee returns. Mutual fund investments are subject to market risk. However, SIP reduces the risk of bad timing through rupee cost averaging, which means your average purchase cost tends to be lower over time. Historically, long-term SIPs in diversified equity funds have generated strong returns for Indian investors — but past performance is not a guarantee of future results.

Q9. Is it a good time to start SIP in 2026 when markets are high?

One of the most common questions we hear. The honest answer is: the "right time" to start a SIP is almost always now. SIPs are designed specifically to handle high markets — you buy fewer units when prices are high and more when they correct. Waiting for markets to fall before starting a SIP defeats the entire purpose of the strategy.

Q10. What is rupee cost averaging in SIP?

Rupee cost averaging is the mechanism by which SIP investors automatically buy more mutual fund units when the market is low and fewer units when the market is high. Over time, this brings down the average cost per unit. It's one of the key reasons why SIP is considered a low-risk investment strategy compared to lumpsum, especially for retail investors who can't track markets daily.

Q11. Which is better — SIP or lumpsum for tax saving (ELSS)?

Both work for ELSS (Equity Linked Saving Scheme) investments. However, with SIP in ELSS, each monthly instalment has its own 3-year lock-in period. With lumpsum in ELSS, the entire amount is locked in for 3 years from the date of investment. For someone who wants to start small and save tax regularly, SIP in ELSS makes more sense. For someone deploying a bonus before March 31st for tax saving, lumpsum works better.

Internal Link: ELSS Funds Guide — Finoda | Tax-Saving Investments

Q12. Can NRIs invest via SIP or lumpsum in India?

Yes. NRIs can invest in Indian mutual funds — both via SIP and lumpsum — subject to certain compliance requirements. Investments need to be routed through an NRE or NRO account. The process is similar to resident Indians, though KYC documentation differs. At Finoda, we can guide NRI clients through the process.

Q13. How do I calculate my SIP returns?

Use a SIP calculator to estimate how your monthly investment will grow based on an expected return rate and time horizon. For example, ₹5,000/month at 12% annual returns over 20 years would grow to approximately ₹49.9 lakh. Real returns vary based on market conditions, but this gives you a useful planning benchmark.

Internal Link: Finoda SIP Calculator — Free Tool

Q14. What is STP (Systematic Transfer Plan) and how does it relate to SIP vs lumpsum?

An STP is a middle-ground strategy. You park a large lumpsum in a liquid or debt fund, then transfer a fixed amount from that fund into an equity fund every month — similar to how a SIP works. This is especially useful if you've received a windfall and want to invest it in equity over 12–18 months without the full lumpsum timing risk.

Q15. Does Finoda help with both SIP and lumpsum investments?

Yes. At Finoda, we guide investors across both strategies based on their financial situation, goals, and risk tolerance. We do not push one route over another — our job is to find what works best for you. Whether you're starting a ₹500/month SIP or investing ₹5 lakh as a lumpsum, we're here to help.

Internal Links: