Start SIP from ₹500/Month — Best SIP Plans India 2026 | AMFI-Registered Finoda

A Systematic Investment Plan — or SIP — is one of the most straightforward ways to build real wealth in India. You pick an amount. You pick a date. And you invest it every month into a mutual fund of your choice. That's really it.

We've helped thousands of investors across Bangalore start their SIP journey — many of them with as little as ₹500 a month. Some didn't know what a mutual fund was when they walked in. Most of them now have a corpus they're genuinely proud of.

So if you've been sitting on the fence, this page is written for you.

Already know what you want? Jump straight to our SIP Calculator and see what your monthly investment can become.

What is SIP? — Systematic Investment Plan Explained Simply

SIP stands for Systematic Investment Plan. It's a method where you invest a fixed sum — say ₹1,000 or ₹5,000 — into a mutual fund at regular intervals, typically once a month.

Think of it like an EMI — but in reverse. Instead of paying for something you've already bought, you're building something for your future, one instalment at a time.

Here's what makes it work: you don't need the markets to be "at the right level" to start. In fact, that's the whole point. You invest whether the market is up or down. Over time, this averages out your purchase cost and reduces the impact of short-term volatility. This is called rupee cost averaging, and we'll explain it in detail below.

SIP is not just a product — it's a habit. And habits, as we all know, are what build wealth over the long run.

SIP kya hota hai? If you're wondering in simple terms: SIP ek aisa tarika hai jisme aap har mahine ek fixed amount mutual fund mein invest karte ho. Market upar ho ya neeche — aapka SIP chalta rehta hai.

Want to understand how SIP compares to lumpsum investing? Read our full guide on SIP vs Lumpsum.

Benefits of SIP Investing — Why Every Indian Should Start Now

The numbers don't lie. According to AMFI data, monthly SIP inflows in India crossed ₹31,002 crore in December 2026 — the highest level ever recorded. Over 9.79 crore SIP accounts are active right now across India. That's not a fad. That's a generation of Indians making smarter financial decisions.

But statistics aside, let's talk about what SIP actually does for you.

Rupee Cost Averaging — Profit Even in Market Dips

Most people panic when the market falls. SIP investors, however, do something counterintuitive — they actually benefit from the dip.

Here's why: when the NAV (Net Asset Value) of your fund falls, your fixed monthly amount buys more units. When markets recover, those extra units are worth more. Over time, this lowers your average cost per unit and improves your returns.

In our experience, this is one of the most powerful mental and financial advantages of SIP. It removes the guesswork. You don't have to time the market. The market timing, in a sense, works for you automatically.

Understanding NAV and fund categories? Visit our Mutual Funds Guide.

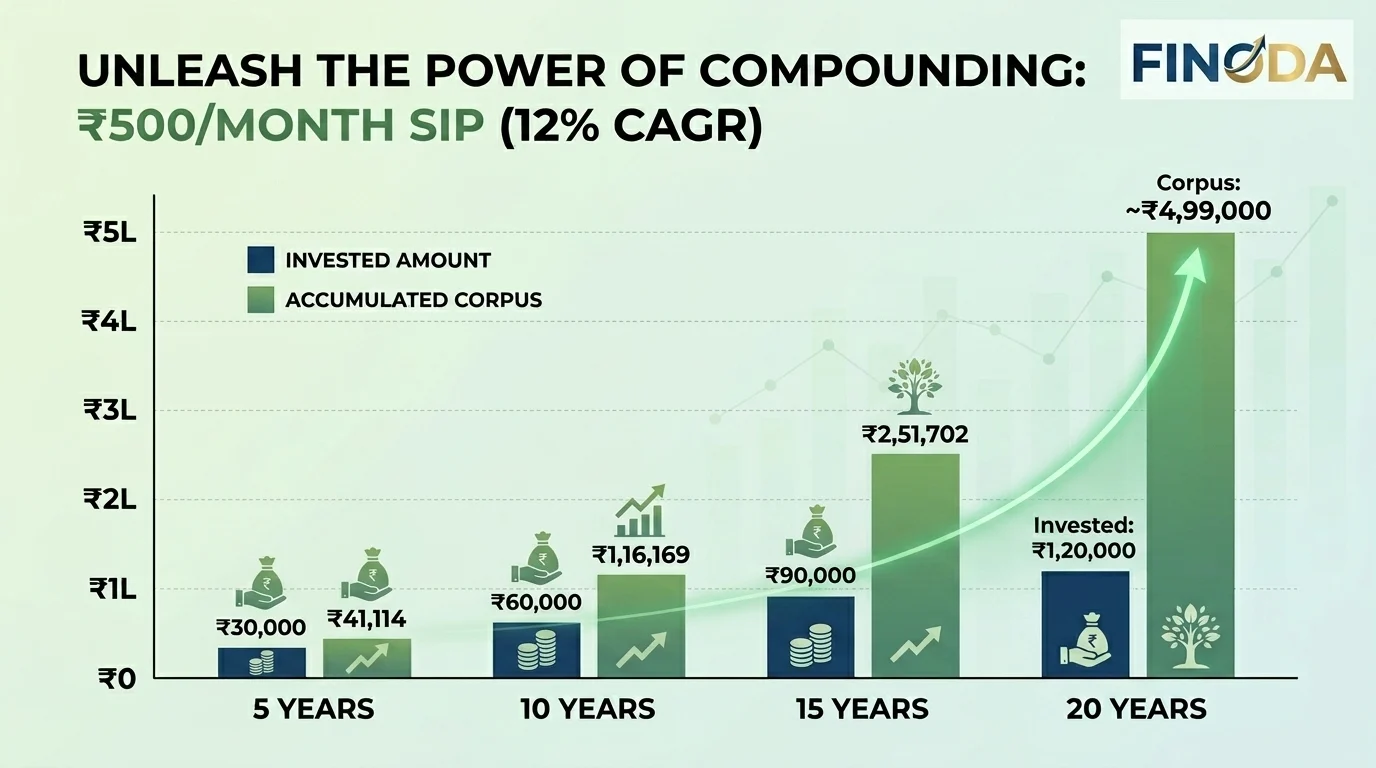

Power of Compounding — How ₹500/Month Becomes ₹10 Lakh

Here's a calculation that surprises most first-time investors:

If you invest ₹500 per month for 20 years at a CAGR of 12%, your total invested amount is just ₹1.2 lakh — but your corpus grows to approximately ₹4.97 lakh. Push the rate to 15% (historically achievable in good equity funds over long tenures), and you're looking at closer to ₹7.5 lakh from just ₹500 a month.

Now scale that up. A ₹5,000/month SIP over 20 years at 12% CAGR generates a corpus of nearly ₹50 lakh — from a total investment of only ₹12 lakh. The rest is compounding doing its job, quietly, month after month.

But compound interest needs one thing above all else: time. Start today, not "next month." The extra few months make a real difference in your final corpus.

Run your own numbers on our SIP Calculator and see the compounding effect for yourself.

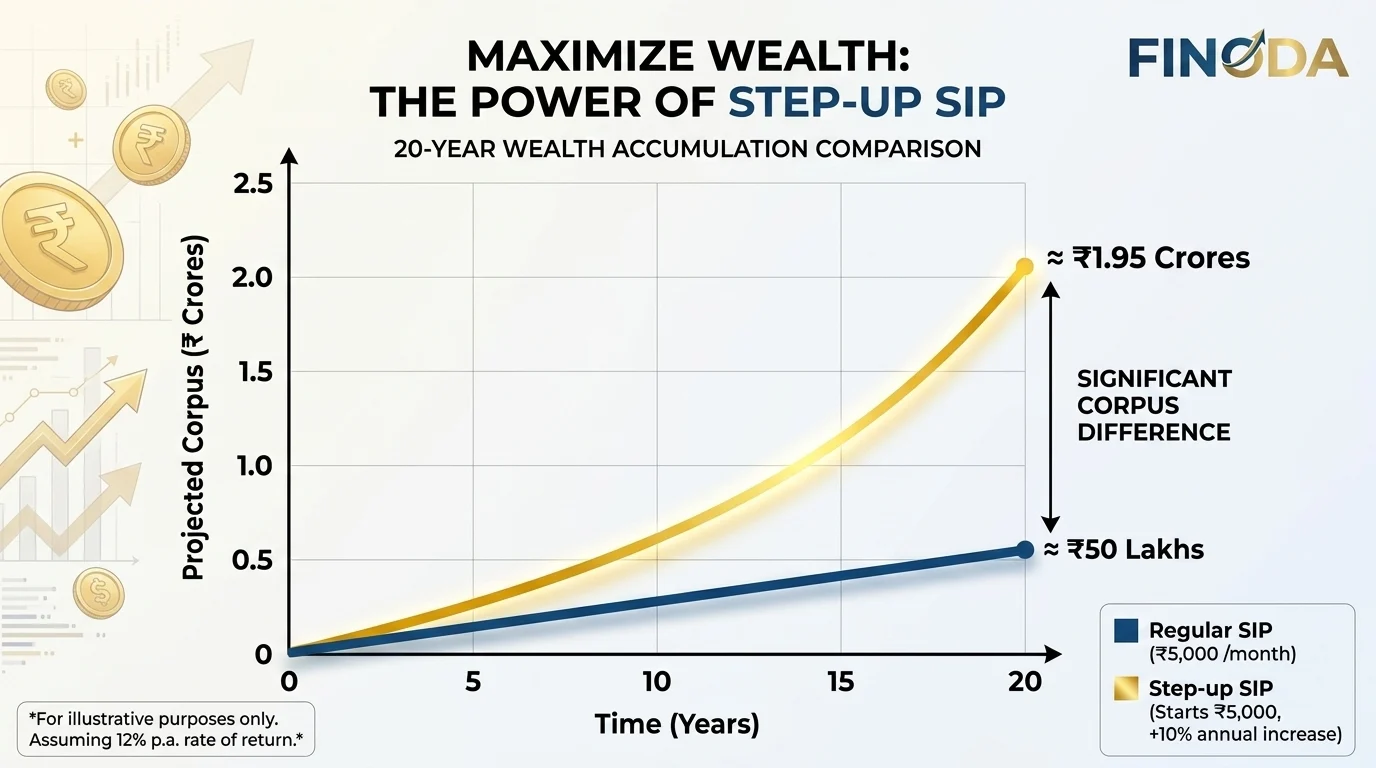

Step-Up SIP — Increase Your Investment Every Year

Most of us get a salary hike every year. Step-Up SIP — also called Top-Up SIP — lets your investments grow at the same pace.

With Step-Up SIP, you set a fixed percentage or amount by which your monthly SIP increases every year. For example: start at ₹5,000/month, and increase by 10% annually. By year 10, you're investing ₹12,968/month — and your final corpus is dramatically higher than a flat ₹5,000/month would produce.

We've found that Step-Up SIP is especially popular among salaried professionals in Bangalore's tech and corporate sectors. It matches how incomes actually grow — gradually and consistently.

Try Step-Up scenarios in our SIP Calculator — it supports step-up projections.

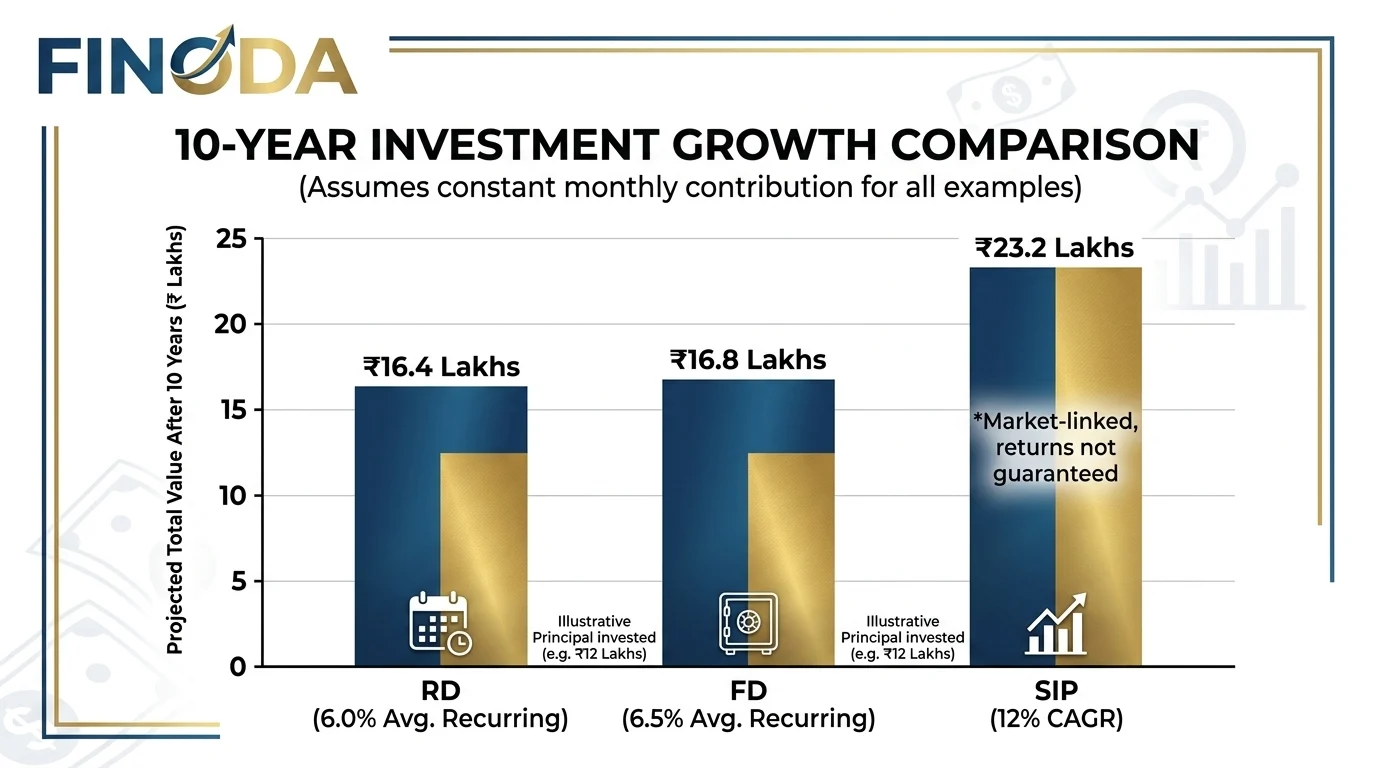

SIP vs FD vs RD — Which is the Better Investment?

This is one of the most common questions we get at Finoda — and honestly, it's a fair one. Fixed Deposits feel safe. RDs feel disciplined. So why choose SIP?

Let's break it down clearly.

| Feature | SIP (Equity Mutual Fund) | FD (Fixed Deposit) | RD (Recurring Deposit) |

|---|---|---|---|

| Average Returns (10-yr) | 12–14% CAGR (historical) | 6.5–7% p.a. | 6–6.5% p.a. |

| Risk | Market-linked | Zero risk | Zero risk |

| Liquidity | High (exit anytime) | Penalty on early exit | Penalty on early exit |

| Tax on Returns | LTCG at 12.5% (>₹1.25 lakh gain) | Taxed as income | Taxed as income |

| Minimum Amount | ₹500/month | ₹1,000+ | ₹100/month |

| Inflation Protection | Strong | Weak | Weak |

So which should you pick? Honestly — that depends on your goals, time horizon, and risk appetite. If you're saving for 3–5+ years and can tolerate some short-term volatility, equity SIPs have historically outperformed both FD and RD by a significant margin. For short-term goals under 1–2 years, an FD is perfectly sensible.

We've seen investors at Finoda use both — FD for emergencies, SIP for long-term wealth. There's no law that says you have to pick just one.

Explore Fixed Deposit investments through Finoda as well.

Check AMFI's official SIP industry data at amfiindia.com for unbiased reference.

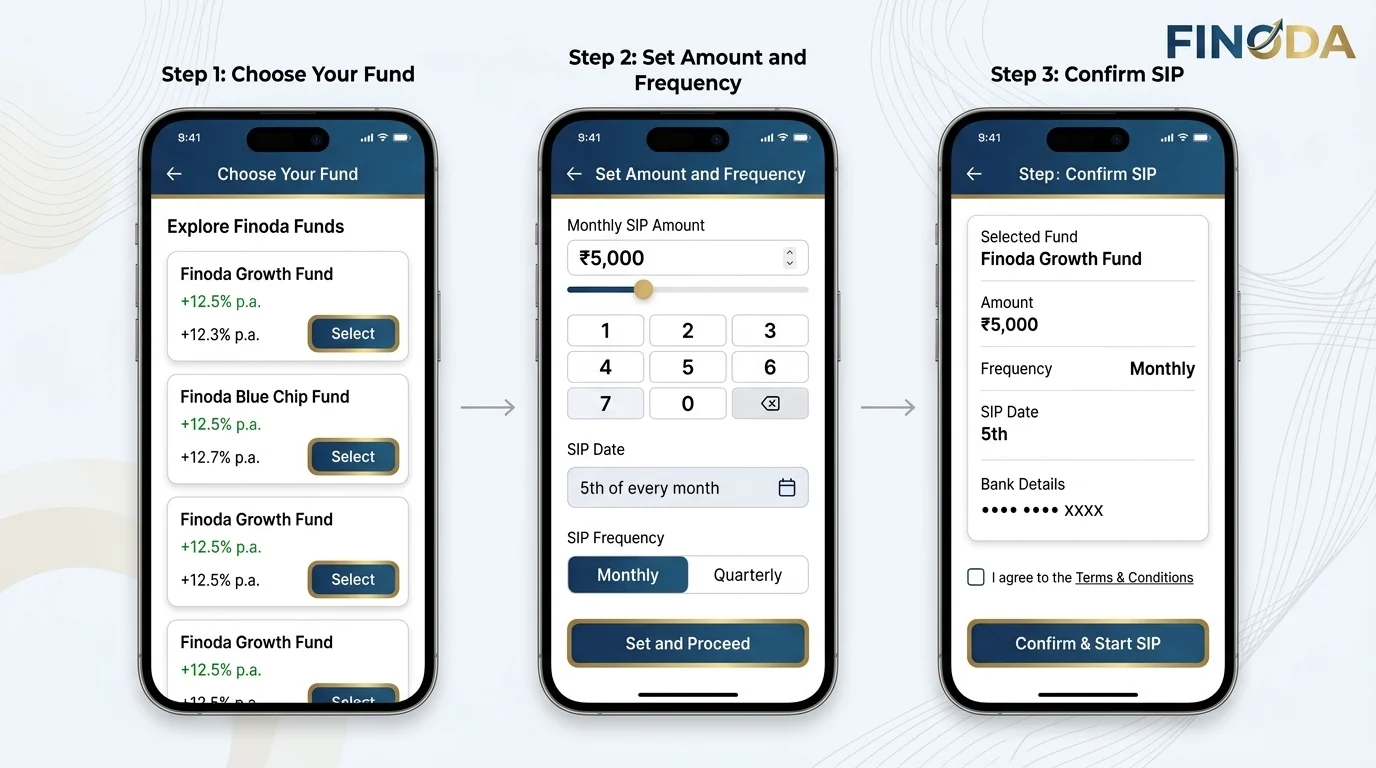

How to Start SIP Online with Finoda in 3 Simple Steps

Starting a SIP with Finoda takes about 10 minutes. Here's exactly how it works.

That's it. No complicated paperwork. No confusing dashboards. Just a clean, guided process.

Ready to begin? Open your Demat Account with Finoda — it's free and takes under 15 minutes.

Best SIP Plans in India 2026 — Expert-Selected Funds

We don't just hand you a list and walk away. At Finoda, our advisors actively track fund performance, expense ratios, fund manager quality, and category alignment. The funds below represent categories our team finds consistently strong for long-term SIP investing.

| Fund Category | Who It's For | Risk Level | Ideal SIP Tenure |

|---|---|---|---|

| Large Cap Funds | Conservative equity investors | Moderate | 5+ years |

| Flexi Cap Funds | Those who want fund managers to decide allocation | Moderate-High | 7+ years |

| Mid Cap Funds | Investors comfortable with higher volatility | High | 7–10+ years |

| ELSS (Tax-Saving Funds) | Anyone wanting 80C deduction + equity growth | Moderate-High | 3+ years (lock-in) |

| Index Funds (Nifty 50) | Passive investors, low cost preference | Moderate | 5–10+ years |

Want to go deeper? Read our ELSS Funds Guide for a complete breakdown of tax-saving SIP options.

Also explore our full Mutual Funds section for more fund categories.

The right fund for you isn't necessarily the one with the highest returns over the last year. We've found that fund consistency, expense ratio, and category suitability matter far more over a 10-year SIP journey.

SIP in India — The Numbers Speak for Themselves

We want to share some real data, because it helps put things in perspective.

According to AMFI:

- Monthly SIP inflows in India crossed ₹31,002 crore in December 2026 — the highest level in history.

- SIP contributions for the full year 2026 crossed ₹3 trillion — the first time this milestone was reached in a single year.

- As of December 2026, 9.79 crore SIP accounts are active across India.

- SIP AUM reached ₹16.63 lakh crore by end of 2026 — over 20% of the entire mutual fund industry's assets.

- Year-on-year SIP contributions grew by 20% in August 2026 alone — from ₹23,547 crore to ₹28,265 crore.

These numbers tell a clear story. Indian investors — especially younger ones — are choosing SIP as their primary wealth-building tool. The habit of regular investing is no longer something only financial experts talk about. It's mainstream.

Data sourced from the AMFI Monthly Notes — India's official mutual fund industry body.

Frequently Asked Questions — SIP Investing India

FAQ 1: What is SIP investing?

SIP (Systematic Investment Plan) is a method of investing a fixed amount regularly — usually monthly — into a mutual fund. It promotes disciplined investing regardless of market conditions and benefits from rupee cost averaging and compounding over time.

FAQ 2: Can I stop SIP anytime?

Yes. Most mutual fund SIPs can be paused for 1–3 months or cancelled entirely without any penalty or charges. Simply log in to your Finoda account or call our advisory team, and we'll handle the paperwork for you.

FAQ 3: What happens if I miss a SIP instalment?

Missing one SIP instalment doesn't attract a penalty in most mutual funds. However, your bank may charge a nominal failed auto-debit fee (usually ₹25–500). If you miss 2–3 consecutive instalments, some fund houses may automatically cancel the SIP. It's always best to pause it officially if you know you'll miss a payment.

FAQ 4: Is SIP better than FD (Fixed Deposit)?

Historically, equity mutual fund SIPs have generated 12–14% CAGR over 10+ year periods, compared to 6–7% from bank FDs. However, SIPs are market-linked and carry risk, while FDs offer guaranteed returns. The right choice depends on your time horizon, risk appetite, and financial goals. For goals 5 years or more away, equity SIPs have consistently outperformed FDs after tax and inflation.

FAQ 5: What is a step-up SIP?

Step-up SIP (also called Top-Up SIP) lets you increase your SIP contribution by a fixed amount or percentage every year. For example, you can start at ₹5,000/month and increase it by 10% each year. This is especially useful for salaried professionals who receive annual increments — your SIP grows with your income.

FAQ 6: What is the minimum SIP amount in India?

The minimum SIP amount varies by fund house, but many mutual funds now allow SIPs starting at ₹100–₹500 per month. At Finoda, we help investors start from ₹500/month, making SIP investing genuinely accessible to first-time investors.

FAQ 7: How is SIP different from lumpsum investing?

In a lumpsum investment, you invest a large amount all at once. With SIP, you invest a fixed smaller amount at regular intervals. SIP reduces your dependency on market timing and benefits from rupee cost averaging. Lumpsum can be more effective when you invest at the right market levels, but SIP removes that risk entirely. Most advisors recommend SIP for regular income earners.

FAQ 8: Is SIP safe?

SIP itself is a method of investing — not a product. Its safety depends on the mutual fund you choose. SIPs into large-cap or index funds are considered relatively lower risk among equity options. SIPs into mid or small-cap funds carry higher risk but also higher potential returns. All mutual fund investments carry market risk.

FAQ 9: Can I invest ₹1,000 per month in SIP?

Absolutely. ₹1,000 per month is a very common starting point. At 12% CAGR over 10 years, a ₹1,000/month SIP can grow to approximately ₹2.32 lakh — from a total investment of just ₹1.2 lakh. Over 20 years, that same ₹1,000/month reaches roughly ₹9.99 lakh. The key is to start early and stay consistent.

FAQ 10: What is SIP kya hota hai bank mein?

SIP is not directly a bank product — it's a mutual fund investment method. However, most banks in India offer SIPs through their in-house mutual fund platforms. Alternatively, you can invest through registered platforms like Finoda, which give you access to multiple fund houses and independent advisory guidance rather than being limited to one bank's offerings.

FAQ 11: Does SIP have a lock-in period?

Most regular SIPs have no lock-in period — you can redeem your units anytime. However, ELSS (Equity Linked Savings Scheme) SIPs come with a mandatory 3-year lock-in per instalment for tax benefits under Section 80C. Each SIP instalment in ELSS completes its own 3-year lock-in from its date of investment.

FAQ 12: How do I choose the best SIP plan for me?

The "best SIP plan" depends on three things: your investment goal, your time horizon, and your risk tolerance. A 25-year-old saving for retirement in 30 years can take more risk than a 45-year-old saving for their child's education in 5 years. Our advisors at Finoda do a detailed goal-mapping session before recommending any fund — because one size truly doesn't fit all in SIP investing.

FAQ 13: What is the SIP amount for ₹1 crore in 20 years?

To reach ₹1 crore in 20 years at a 12% CAGR, you would need to invest approximately ₹10,011 per month through SIP. If you use a Step-Up SIP starting at ₹5,000 and increasing 10% annually, you can reach the same goal with a lower starting amount. Use our SIP Calculator to model your exact scenario.

Have more questions? Visit our Main FAQ Page for comprehensive answers across all investment topics.

Why Choose Finoda for Your SIP?

Here's what makes us different from opening a SIP through a random app or your bank's portal.

First, we're independent. We're not tied to selling you one fund house's products. Our AMFI-registered advisors give you recommendations based on your specific goals — not on commission structures or product quotas.

Second, we're local. We're based in Bangalore, at HAL Old Airport Road. If you want to sit across a table and have a real conversation about your finances — we're here for that. Not just on a chatbot.

Third, we stay with you. SIP is a long-term journey, and markets go through rough patches. We've seen investors panic and redeem at the wrong time — we actively work to prevent that. Our advisory relationship doesn't end after you start the SIP.

Read about our full service philosophy on our Why Choose Finoda page.

Also explore NPS Investment as a long-term retirement complement to SIP.