Long-Term Investing India — Build Wealth Through an Expert-Guided Portfolio

Long-term investing is one of the most reliable paths to building real wealth in India. It means buying quality assets — equity stocks, mutual funds, or index funds — and holding them for 5, 10, or even 20 years. No daily screen-watching. No panic selling. Just letting your money grow through the power of compounding.

At Finoda, we've helped thousands of investors in Bangalore and across India build portfolios that work quietly in the background — while they focus on their careers, families, and lives.

Why Long-Term Investing Beats Short-Term Trading

Most people come to us after trying intraday trading. And honestly? We don't judge. The idea of making money every day sounds exciting. But here's what the data actually shows: a SEBI study released in July 2025 confirmed that 91% of individual F&O traders lost money in FY 2024-25. Not a few. Not the unlucky ones. Nine out of ten.

Long-term investing works the opposite way. You're not trying to time the market. You're giving the market time.

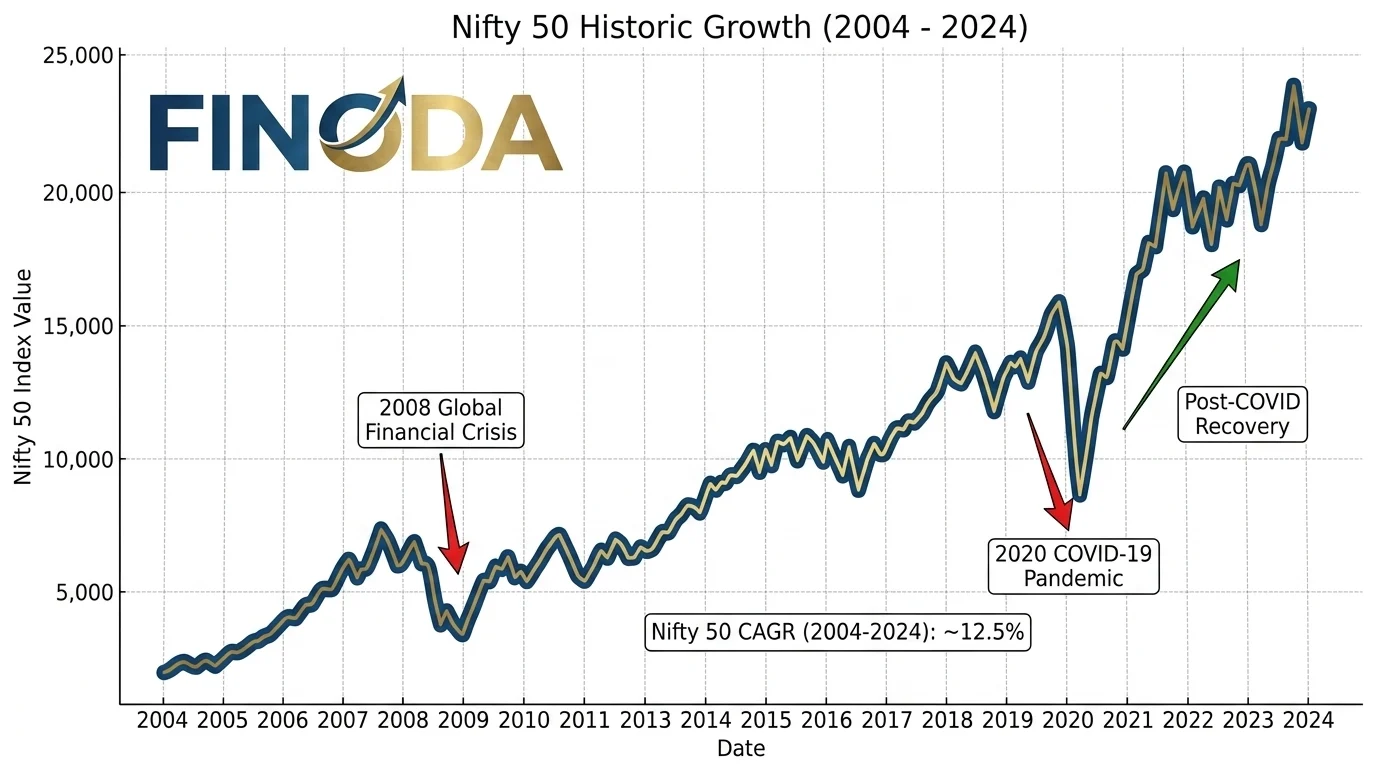

We've found that investors who stay invested through market dips — the 2008 financial crisis, the 2020 COVID crash, the 2022 rate-hike correction — consistently come out ahead. The short-term investor who exited in March 2020 locked in a 40% loss. The long-term investor who held through it saw the Nifty 50 recover and then reach all-time highs within 18 months.

So why does short-term trading feel more tempting? Because our brains crave quick results. But in wealth creation, patience is the actual edge — and it's one that most retail investors underuse.

Nifty 50 Has Returned ~12.82% CAGR Since Inception — Here's How to Benefit

Numbers matter in investing. So let's look at what the Indian market has actually delivered — not projections, not best-case scenarios. Real, historical data.

As of 30 September 2025, the Nifty 50 Index has delivered an annualised return of 12.82% since its inception in April 1996. The 10-year SIP XIRR has been 14.0%. That's through wars, recessions, rate hikes, demonetisation, and a pandemic. Through all of it.

To put that in practical terms: if you had invested ₹10,000/month in a Nifty 50 index fund via SIP starting 10 years ago, your investment would have grown to approximately ₹24.95 lakh. Your total contribution? Around ₹12 lakh. The market did the rest.

And this isn't a cherry-picked example. It's the result of systematic, disciplined, long-term investing — exactly what we help our clients do at Finoda.

But knowing the history isn't enough. What matters is having a structure in place — the right fund selection, the right asset allocation, and someone to call when the market drops 20% and your gut tells you to sell. That's where we come in.

Long-Term Investment Options Available at Finoda

We don't believe in one-size-fits-all portfolios. Different people have different goals, timelines, and risk appetites. So here's what we actually offer — with honest notes on each.

Equity Stocks — Direct Ownership in India's Growth Story

Direct equity is our bread and butter. Through our platform, you get access to NSE and BSE-listed stocks — everything from large-cap blue chips to mid-cap growth stories. We help you build a diversified stock portfolio based on your investment horizon and goals.

Our team follows a buy-and-hold philosophy for long-term portfolios. We're not chasing quarterly earnings surprises. We're looking for companies with strong fundamentals, a durable competitive advantage, and management we trust.

Mutual Funds — Professional Management, Lower Effort

Not everyone wants to pick individual stocks. And that's completely fine. Mutual funds give you professional fund management, built-in diversification, and the ability to start small — even ₹500/month.

We help our clients choose between large-cap, flexi-cap, mid-cap, and ELSS funds based on their specific situation. Moreover, we don't earn commissions by pushing you toward high-expense funds. Our advice is based on what fits you.

SIP — Systematic Investing for Salaried Professionals

If you're a salaried professional in Bengaluru, SIP is probably your best tool. You invest a fixed amount monthly — ₹1,000, ₹5,000, ₹25,000 — and the platform does the rest automatically.

The benefit isn't just convenience. SIPs average out your cost of purchase across market cycles, which means you buy more units when prices are low and fewer when they're high. Over a 10- or 20-year period, this rupee cost averaging adds up significantly.

ELSS — Tax Savings + Equity Growth

ELSS (Equity Linked Savings Schemes) funds give you a Section 80C deduction of up to ₹1.5 lakh per year while keeping your money invested in equity. The lock-in period is only 3 years — the shortest among all 80C options. It's an overlooked gem for first-time equity investors.

NPS — National Pension System for Retirement Planning

NPS is underused and underrated. It's a market-linked retirement product with one of the lowest expense ratios of any investment vehicle in India. Additionally, you get additional tax deductions under Section 80CCD(1B) — over and above the ₹1.5 lakh 80C limit.

We've found that NPS works best as a complement to equity, not a replacement. We help you decide the right equity-debt split based on your age and retirement timeline.

Building Your Long-Term Portfolio — Asset Allocation Guide

Asset allocation is the most important decision in long-term investing. More important than fund selection. More important than market timing. And yet, most investors skip it.

Here's a simple framework we use at Finoda:

- Equity (Growth engine): 60–80% for investors under 40. Equity delivers the highest long-term returns, but it comes with short-term volatility. If you have 10+ years ahead, that volatility is actually your friend — it lets you buy more units when markets dip.

- Debt (Stability layer): 15–30% in debt instruments — whether that's debt mutual funds, fixed deposits, or corporate bonds. Debt cushions your portfolio when equity falls sharply.

- Gold (Hedge): 5–10% in gold, ideally through Sovereign Gold Bonds or Gold ETFs. Gold tends to do well when equity struggles, which makes it a good hedge in a diversified portfolio.

The exact mix depends on your age, income, liabilities, and risk tolerance. We sit down with you and work this out — not on a standard template, but based on your actual financial picture.

How Compounding Creates Wealth Over Time

Einstein reportedly called compound interest the eighth wonder of the world. Whether or not he actually said that — the math checks out.

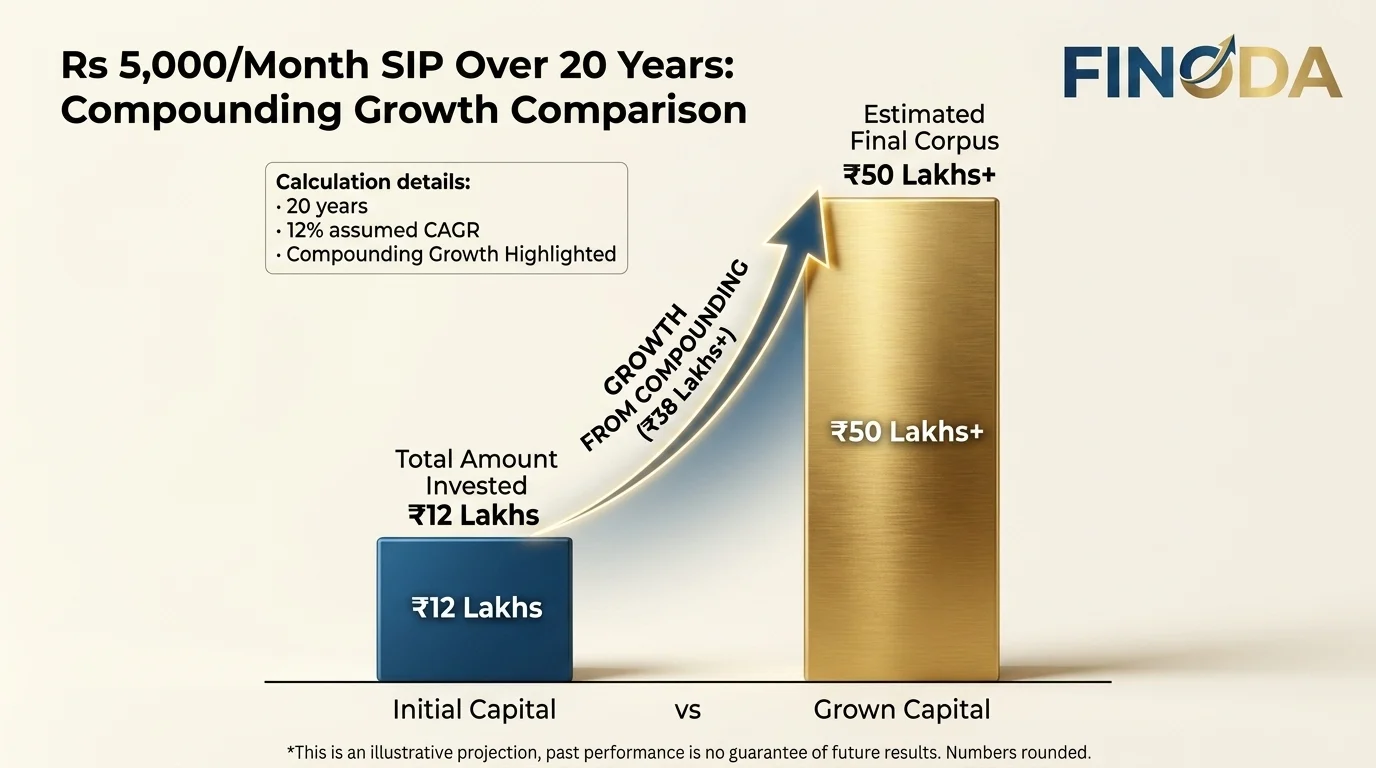

Here's a real example. If you invest ₹5,000 every month in an equity mutual fund through SIP, and the fund delivers 12% CAGR over 30 years: your total investment is just ₹18 lakh. But your final corpus? ₹1.76 crore. That's not financial magic. That's arithmetic working in your favour over time.

The key insight is this: in the early years, compounding is slow. In the later years, it accelerates dramatically. The last 5 years of a 30-year SIP often generate more wealth than the first 20. This is why starting early matters more than investing large amounts.

We've seen this first-hand with our clients. The ones who started a ₹3,000 SIP at age 25 are in far better shape at 45 than clients who started a ₹10,000 SIP at age 35. Time in the market beats timing the market. Every single time.

Want to see your own numbers? Use our SIP Calculator or Lumpsum Calculator to run projections based on your investment amount and timeline.

Start Your Long-Term Wealth Journey with Finoda

Getting started is simpler than most people think. Here's how we do it:

Step 1 — Free Consultation. We sit down with you (in-person or online) and understand your goals, income, existing liabilities, and risk comfort. No pressure. No sales pitch.

Step 2 — Portfolio Design. Based on your profile, we recommend a specific allocation — which funds, which stocks, what split, and why. You always know the reasoning behind every recommendation.

Step 3 — Account Opening. If you don't already have a demat account, we help you open one. It takes about 15–20 minutes online.

Step 4 — SIP / Investment Setup. We set up your SIPs or one-time investments and make sure everything runs automatically. You don't need to log in every month.

Step 5 — Annual Review. Every year, we review your portfolio together — rebalance if needed, adjust SIP amounts if your income has grown, and make sure you're on track for your goals.

That's it. No complexity. No jargon. Just a clear plan executed consistently.

Frequently Asked Questions (FAQs)

Long-term investing means putting money into assets like equity stocks, mutual funds, or index funds — and holding them for at least 5 years, ideally 10 or more. The goal is to benefit from India's economic growth and the power of compounding. Unlike short-term trading, you're not watching prices daily. You're giving your investments time to compound and grow.

The Nifty 50 has delivered approximately 12.82% CAGR since its inception in April 1996. Over the last 10 years, a systematic SIP investor would have earned around 14% XIRR. These returns significantly outperform traditional fixed deposits (6–7% per annum) and gold over the same periods.

No investment is "risk-free" — but long-term equity investing in India has historically been far more rewarding than most alternatives when held for 7+ years. The key risk is short-term volatility. If you need the money within 2–3 years, equity is not ideal. But for 10-year-plus goals, equity has historically delivered positive real returns in India across every 10-year rolling window.

You can start a SIP with as little as ₹500 per month. For direct equity, most brokers allow stock purchases from ₹1 onwards. The amount matters less than the habit of starting. We always tell our clients: start with what you can sustain, and increase it as your income grows.

Both work well for long-term investing. SIP is better if you have a regular monthly income and want to average out market volatility. Lumpsum works better when markets have seen a significant correction and valuations are attractive. In practice, most of our clients use SIP as their default approach and deploy lumpsum amounts during sharp market dips.

Based on our experience, a diversified approach works best:

- Equity mutual funds (flexi-cap or large-cap index funds for lower risk)

- ELSS funds (for Section 80C tax savings with equity upside)

- NPS (for retirement-focused long-term investing with additional tax benefits)

- Direct equity in quality large-cap and mid-cap companies

- Sovereign Gold Bonds as a 5–10% hedge

The right mix depends on your age, income, goals, and risk comfort — something we help you work out in a one-on-one consultation.

For equity mutual funds and listed stocks held for more than 1 year, gains are classified as Long-Term Capital Gains. As of the current tax rules, LTCG above ₹1.25 lakh per year is taxed at 12.5% (without indexation). This is still far lower than short-term gains (20%) and significantly lower than your income tax slab rate. For most investors, LTCG tax reduces post-tax CAGR by roughly 1–1.5%.

Yes. Through Finoda's platform, you can invest in Nifty 50 stocks individually or buy Nifty 50 index funds via SIP or lumpsum. We help you decide whether direct stocks or index funds suit your investment style better — and why that distinction matters for your specific situation.

Intraday trading means buying and selling stocks within the same trading day. You need to monitor prices constantly, understand technical analysis, and manage significant stress. According to SEBI's 2025 study, 91% of individual F&O traders lost money in FY 2024-25.

Long-term investing means buying quality assets and holding them for years. It requires less daily attention, benefits from India's economic growth over time, and historically delivers better risk-adjusted returns for most retail investors.

A common starting point for someone in their 30s: 70% equity (mutual funds or direct stocks), 20% debt (debt funds or FD), and 10% gold (Sovereign Gold Bonds or Gold ETF). As you get closer to retirement, you gradually shift more toward debt to reduce volatility. We help you design and maintain this allocation as your life situation changes.

SIP (Systematic Investment Plan) works through two mechanisms: rupee cost averaging and compounding. Rupee cost averaging means you buy more units when prices are low and fewer when they're high — automatically. Over 10–20 years, this smooths out market volatility significantly. Compounding means the returns you earn start generating their own returns. A ₹5,000/month SIP at 12% CAGR for 30 years grows to ₹1.76 crore — on a total investment of just ₹18 lakh.

ELSS (Equity Linked Savings Scheme) is an equity mutual fund that qualifies for Section 80C deduction up to ₹1.5 lakh per year. It has a lock-in period of just 3 years — shorter than PPF (15 years) or NSC (5 years). It's invested primarily in equity, so the growth potential is higher than most other 80C options. We consider ELSS a smart choice for investors who want to save tax and grow wealth at the same time.

Direct equity suits investors who have time to research individual companies, understand financial statements, and stay patient through stock-specific volatility. Mutual funds suit investors who want diversification without stock-picking effort — a fund manager handles the selection. In our experience, most first-time investors do better starting with mutual funds and gradually learning equity as their comfort grows.

Absolutely not. Investing at 40 with a 20-year horizon still gives compounding significant room to work. Someone who starts a ₹15,000/month SIP at 40 and stays invested for 20 years at 12% CAGR would accumulate approximately ₹1.5 crore. Moreover, at 40, you often have a higher income and lower lifestyle inflation — which means you can invest more aggressively than you could in your 20s.

Yes. Finoda operates under SEBI guidelines, and all investment transactions are executed through regulated platforms. Your securities are held with CDSL or NSDL depositories — not with us directly. We follow all applicable compliance requirements to ensure your investments are safe and transparently managed.