Expert Income Tax Filing Services India 2026 — CA-Assisted ITR

Filing income tax returns can feel like a mess — confusing forms, changing rules, missed deductions, and a hard deadline staring at you. We've helped thousands of salaried employees, business owners, freelancers, and investors across Bangalore and pan-India file their ITR accurately and on time.

At Finoda, we don't just punch your numbers into a portal. Our CA team reviews your actual income, investments, and deductions — then files the right form for you. We handle ITR-1, ITR-2, ITR-3, and ITR-4, and we start at ₹499.

Filing season for FY 2025-26 (AY 2026-27) is now open. The deadline for salaried taxpayers (ITR-1, ITR-2) is 31 July 2026. Don't wait till the last week.

Table of Contents

ITR Filing Last Date India 2026 — Don't Miss These Deadlines

The Central Board of Direct Taxes confirmed the following deadlines for FY 2025-26 (AY 2026-27). These are the real, updated dates — not estimates.

| Taxpayer Category | ITR Forms | Due Date |

|---|---|---|

| Individuals, salaried, HUF (no audit) | ITR-1, ITR-2 | 31 July 2026 |

| Non-audit business / profession cases | ITR-3, ITR-4 | 31 August 2026 |

| Audit cases (companies, partnership firms, etc.) | ITR-3, ITR-5, ITR-6 | 31 October 2026 |

| Transfer pricing cases | ITR-3, ITR-6 | 30 November 2026 |

| Belated / late filing | All | 31 December 2026 |

| Revised return deadline | All | 31 March 2027 |

Missing July 31 attracts a late fee of ₹1,000 (if income ≤ ₹5 lakh) or ₹5,000 (higher income) under Section 234F. Interest at 1% per month also applies on unpaid tax under Section 234A. So filing early is always smarter.

Budget 2026 update: Finance Minister Nirmala Sitharaman announced staggered ITR deadlines in the Union Budget. ITR-1 and ITR-2 stay at July 31. Business/profession cases (ITR-3, ITR-4) now get August 31. Revised returns can be filed until March 31 of the relevant assessment year.

In our experience, most salaried employees wait until mid-July. That last-minute rush means errors, mismatches in AIS, and slower refund processing. We've found that filing before June 30 gets you refunds 3-4 weeks faster.

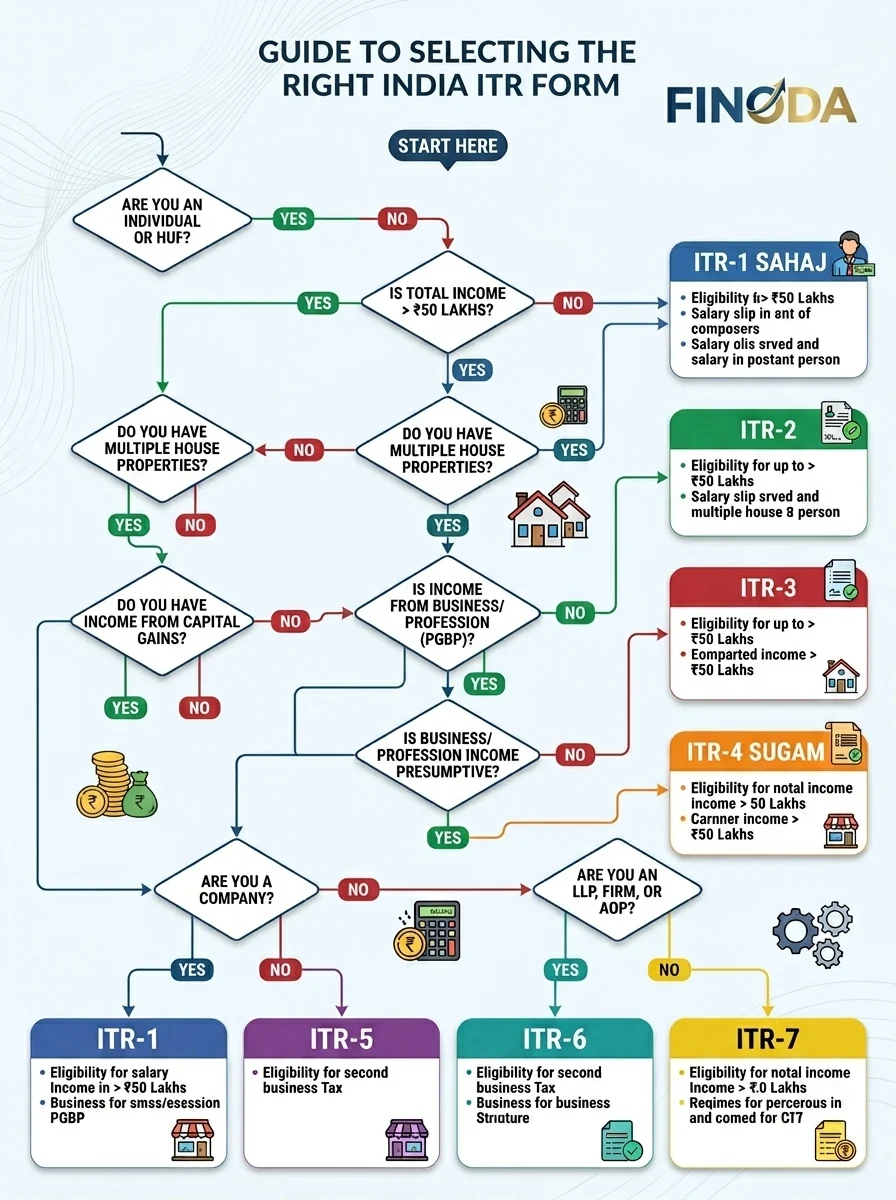

Which ITR Form Should You File? — ITR-1, ITR-2, ITR-3, ITR-4 Explained

This is honestly the most common confusion we hear from clients: "Which form should I use?" The answer depends on your income sources. Here's a quick guide.

ITR-1 (Sahaj) — For Salaried Employees

Who should file ITR-1? Salaried employees with salary income, one house property, and interest income — as long as total income stays below ₹50 lakh. No capital gains allowed, no foreign income, and no business income. This is the simplest form.

Documents you'll need: Form 16 from your employer, Form 26AS, AIS from the income tax portal, and your bank interest certificates. That's broadly it.

In our CA team's experience, around 60-70% of IT professionals in Bangalore fall cleanly into ITR-1. We file most ITR-1 cases within 24-48 hours once documents are submitted. We also verify your AIS carefully — missed TDS credits and mismatches are the single biggest reason for income tax notices.

If you've started investing through Finoda and hold only mutual funds (redeemed before the year ended), or have FD interest — ITR-1 still works for most of you, unless you've sold equity or mutual funds during the year.

Want to open a demat account and start generating 80C deductions through ELSS? We file your ITR the same year, so it's seamless.

ITR-2 — For Capital Gains & Multiple Income Sources

Who should file ITR-2? Anyone with salary income plus capital gains — from stocks, mutual funds, property, or any other capital asset. If you've bought or sold equity shares, mutual funds, or property during FY 2025-26, you'll need ITR-2, not ITR-1.

This is especially relevant for our trading clients at Finoda. Long-term capital gains (LTCG) from equity over ₹1.25 lakh are taxable at 12.5% from FY 2025-26 onwards (post Budget 2024 change). Short-term capital gains (STCG) on equity are taxed at 20%. Our CA files Form 112A for LTCG equity transactions and reconciles it with your broker's capital gains statement.

If you've had capital gains from stock trading or equity delivery, ITR-2 is your form. We reconcile every trade from your broker statement with your AIS, which is something many people skip — and then get notices for later.

ITR-3 — Business, Professional & F&O Income

Who files ITR-3? Business owners, freelancers, consultants, professionals, and F&O traders where F&O income is treated as business income. This is the most comprehensive form — it requires a Profit & Loss account and balance sheet.

F&O trading income tax is one of the trickiest areas. If your F&O turnover crosses the threshold or if you want to carry forward losses (you can carry forward F&O losses for 8 years), a complete P&L from your broker is mandatory. Our CA team handles this — including reconciliation of every contract note, STT deductions, and brokerage charges.

Business owners: ITR-3 is also relevant if you're running a proprietorship or practising as a professional (doctor, lawyer, architect, etc.). We prepare the P&L, balance sheet, and file the return — alongside GST filing services if you're GST-registered.

ITR-4 (Sugam) — Presumptive Income (Small Business & Freelancers)

Who files ITR-4? Small business owners and freelancers who opt for the presumptive taxation scheme under Section 44AD or 44ADA. If your business turnover is below ₹2 crore (or ₹50 lakh for professionals), you can declare a fixed percentage of revenue as income without maintaining detailed books. This is simpler and works well for small traders, retailers, and consultants.

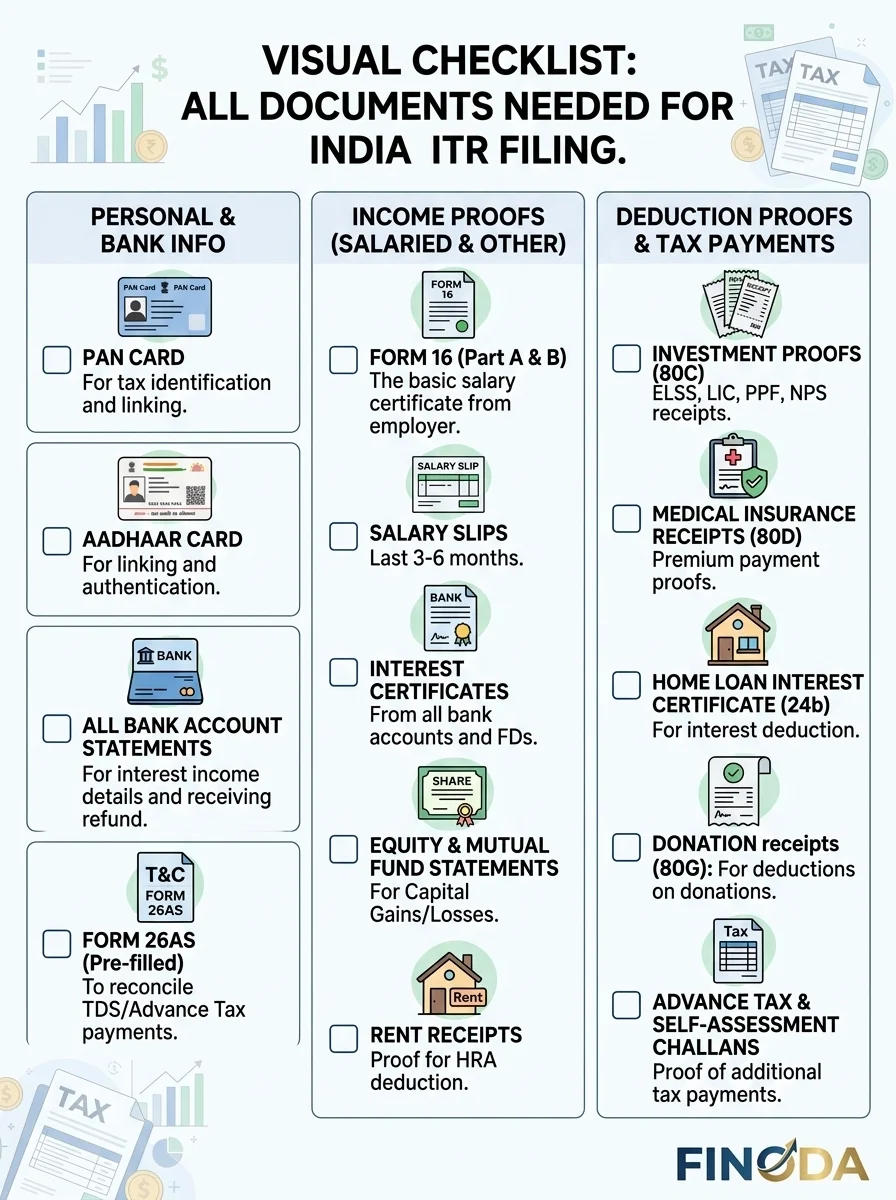

Documents Required for ITR Filing India — Complete Checklist 2026

Getting your documents ready before you speak to us saves time for everyone. Here's what our CA team will ask for, depending on your income type.

For salaried employees (ITR-1 / ITR-2):

- Form 16 (Part A and Part B) from your employer

- Form 26AS — download from income tax portal

- AIS (Annual Information Statement) — also from the income tax portal

- Bank account statements for all savings/salary accounts

- Home loan interest certificate (for 80C and Section 24(b) deduction)

- Investment proofs — ELSS receipts, PPF passbook, NPS contribution statement

- HRA rent receipts (if applicable and not reflected in Form 16)

For capital gains (ITR-2):

- Capital gains statement from your broker (equity + mutual fund)

- Form 112A for equity LTCG if applicable

- Property sale agreement and stamp duty paid (if property was sold)

For business / freelancers (ITR-3 / ITR-4):

- Bank statements (business account)

- GST return summaries (GSTR-1, GSTR-3B)

- P&L account and balance sheet (or turnover details for presumptive cases)

- TDS certificates received from clients (Form 16A)

Tip from our CA desk: Always download your AIS first — not just Form 26AS. The AIS has a far more detailed picture of your financial transactions. Mismatches between AIS and your filed return are the primary reason for income tax notices in recent years. We've found that clients who share their AIS upfront have a much smoother filing experience.

For more on tax-saving investments that generate deduction-eligible documents, check our complete guide.

Section 80C, 80D & Other Deductions — Maximize Your Tax Savings

A lot of people file their ITR without claiming deductions they're fully entitled to. That's money left on the table. Our CA team makes sure you claim every valid deduction — legally, under the old tax regime.

Section 80C (up to ₹1.5 lakh):

- ELSS tax-saving mutual funds — lock-in of 3 years, market-linked returns

- PPF contributions — 15-year lock-in, fully tax-free maturity

- EPF employee contribution — reflected in Form 16

- Life insurance premium

- Tuition fees for children

- Home loan principal repayment

- NSC, SCSS, 5-year tax-saver FD

Section 80CCD(1B) — Extra ₹50,000 via NPS:

NPS for additional 80CCD(1B) deduction gives you an extra ₹50,000 deduction over and above the ₹1.5 lakh 80C limit. For someone in the 30% tax bracket, that's ₹15,000 direct savings every year. It's one of the most underused deductions we see.

Section 80D — Health Insurance:

Premium paid for health insurance for self, spouse, and children: up to ₹25,000. For senior citizen parents: up to ₹50,000. So total 80D can reach ₹75,000 if your parents are senior citizens.

Section 24(b) — Home Loan Interest:

If you have a home loan, interest paid up to ₹2 lakh per year is deductible under Section 24(b) on a self-occupied property.

HRA Exemption:

Salaried employees staying in rented accommodation can claim HRA exemption — the actual calculation involves your actual HRA received, rent paid, and 10% of basic salary. Our CA optimizes this calculation for you.

Section 80E — Education Loan Interest:

Interest on education loans is fully deductible for 8 years from the year of first repayment.

Explore our complete tax-saving investments guide to see where you can invest and simultaneously reduce your tax this year.

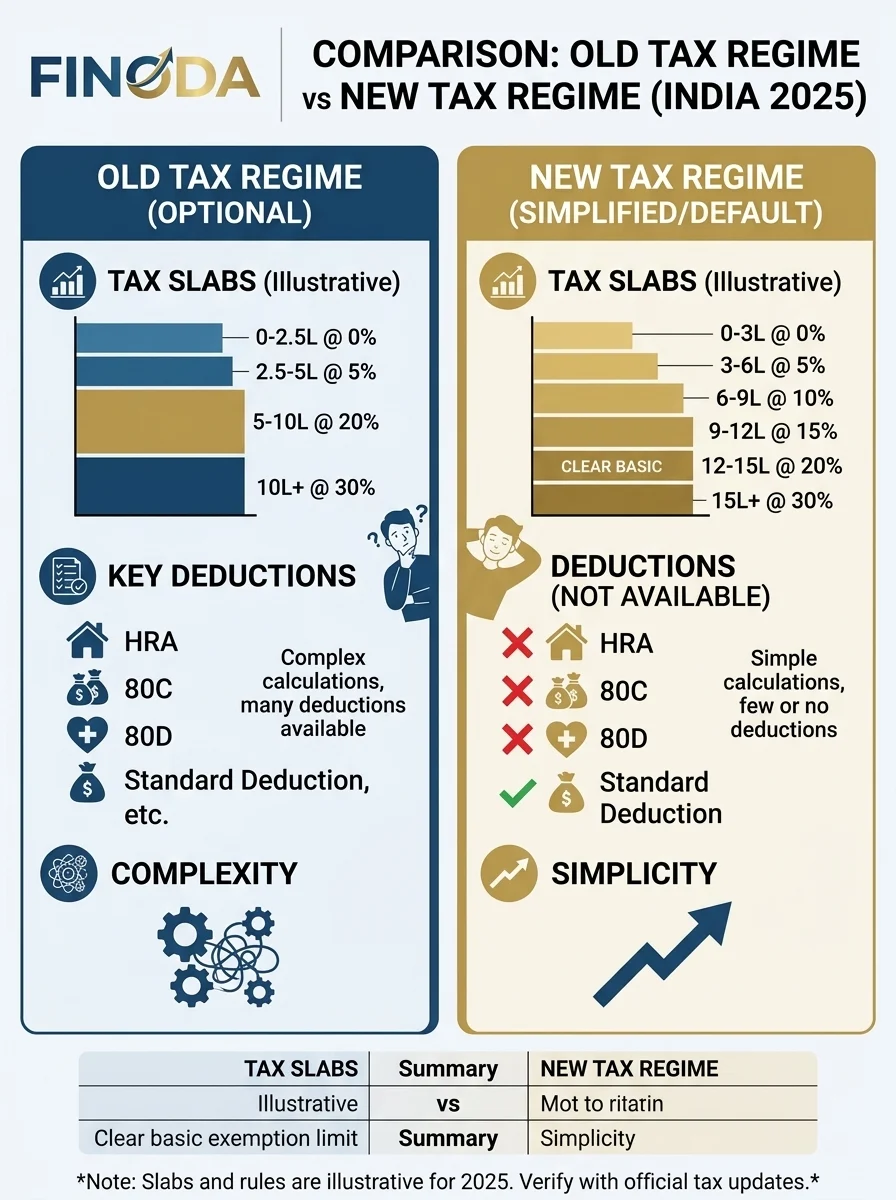

Old Tax Regime vs New Tax Regime 2026 — Which Saves More for You?

This is the question every salaried employee asks us. And the answer genuinely depends on your deductions. But here's a plain comparison first.

New Tax Regime (Default from FY 2024-25 onwards):

| Annual Income | Tax Rate |

|---|---|

| Up to ₹3 lakh | Nil |

| ₹3 lakh – ₹7 lakh | 5% |

| ₹7 lakh – ₹10 lakh | 10% |

| ₹10 lakh – ₹12 lakh | 15% |

| ₹12 lakh – ₹15 lakh | 20% |

| Above ₹15 lakh | 30% |

Under the new regime, income up to ₹12 lakh is effectively tax-free due to the ₹60,000 standard deduction + Section 87A rebate. But you lose all 80C, 80D, HRA, and home loan deductions.

Old Tax Regime:

| Annual Income | Tax Rate |

|---|---|

| Up to ₹2.5 lakh | Nil |

| ₹2.5 lakh – ₹5 lakh | 5% |

| ₹5 lakh – ₹10 lakh | 20% |

| Above ₹10 lakh | 30% |

Higher rates — but all deductions are available.

So which one should you pick?

In our experience, here's a rough breakeven guide:

- Income ₹7-8 lakh: New regime often wins if you have minimal deductions.

- Income ₹10-12 lakh: Old regime wins if you're investing ₹1.5 lakh in 80C + home loan + NPS.

- Income ₹15 lakh+: Old regime almost always wins for disciplined investors claiming full deductions.

- Income above ₹20 lakh with full deductions: Old regime can save ₹50,000-₹1 lakh+ annually.

But these are general rules. The right answer needs actual numbers. Our CA runs the calculation for your specific income and investments before advising you. It takes 10 minutes — and it's part of every filing we do.

How Finoda Files Your ITR — Step-by-Step Process

We don't make you figure out the portal, switch between tabs, or decode your AIS yourself. Here's exactly what happens when you come to us.

Step 1 — Submit Your Documents

Share your documents via our secure client portal — upload Form 16, capital gains statement, bank statements, and investment proofs. Everything stays confidential. You can also WhatsApp us on 9035294343 if you need help gathering documents.

Step 2 — CA Reviews Your Case

Our chartered accountant reviews your income, cross-checks your AIS and Form 26AS, identifies potential discrepancies, and determines the right ITR form for you. This step is where most errors — and most missed deductions — get caught.

Step 3 — Tax Calculation & Deduction Optimization

We run both regimes for you — old and new. We identify every deduction you're entitled to claim. For salaried clients, this includes HRA, 80C, 80D, home loan, and education loan interest. For business clients, we prepare the P&L and optimize allowable expenses.

Step 4 — Client Review & Approval

We share the draft return with you before filing. You review, ask questions, and approve. Nothing goes to the portal without your sign-off.

Step 5 — E-Filing + ITR-V Acknowledgment

Once approved, we file your return on the Income Tax India portal. You receive the ITR-V acknowledgment immediately. For e-verification via Aadhaar OTP or net banking, most cases are verified within minutes.

Typical turnaround: 2-5 business days from document submission. Complex cases (F&O, multiple capital gains, foreign income) may take slightly longer.

Income Tax Filing Charges at Finoda — Transparent Pricing

We believe pricing should be upfront. No surprises after filing. Here's what you pay.

| Return Type | Who It's For | Starting Price | What's Included |

|---|---|---|---|

| ITR-1 | Salaried employees (simple) | ₹499 | CA preparation, review, e-filing, ITR-V acknowledgment |

| ITR-2 | Capital gains, multiple sources | ₹999 | All above + capital gains computation, Form 112A |

| ITR-3 | Business, freelancer, F&O | ₹1,999 | All above + P&L preparation, business income computation |

| ITR-4 | Presumptive business/profession | ₹999 | All above + presumptive income calculation |

| GST + ITR bundle | Business owners | Custom | ITR + GST returns — one advisory team |

Each package includes one revision after filing. Complex cases — foreign income, multiple properties, large capital gains — are quoted separately. Contact us for a free assessment.

Also offering advisory for GST filing services for business owners who want income tax and GST handled by the same team.

Why Finoda for Income Tax Filing?

We're Bangalore-based — so if you work in Koramangala, Whitefield, HSR, Electronic City, or Indiranagar, you're our neighbour. But we file returns pan-India too.

Here's what makes us different from just using a portal or a freelance accountant:

A real CA, not software. Every return is reviewed by a qualified chartered accountant. Portals can prefill data — but they can't tell you whether the old or new regime saves you more, or whether your freelance income needs ITR-3 or ITR-4.

Cross-service advantage. If you trade stocks through Finoda, your capital gains data is already with us. We reconcile it directly. No need to download and re-upload statements. Your equity trading, F&O trades, and ELSS investments — we see the full picture.

Year-round advisory, not just filing. We check in with clients in December-January to review advance tax liability. We run tax projections in March so you know what to expect. It's not a one-time service — it's an ongoing relationship.

Privacy and security. Your documents are handled within a secure client portal. We don't share data with third parties.

Income Tax Filing FAQs — Expert CA Answers

Q1: What is the last date to file ITR for FY 2025-26 (AY 2026-27)?

Q2: Which ITR form should a salaried employee file?

Q3: What documents are required for ITR filing in India?

Q4: Is it mandatory to file ITR if income is below the tax slab?

Q5: How much does ITR filing cost at Finoda?

Q6: What is Form 26AS and AIS in income tax?

Q7: Can I claim ELSS mutual fund investment as 80C deduction in ITR?

Q8: Is F&O trading income reported in ITR? Which form?

Q9: Can I switch from old to new tax regime every year?

Q10: What happens if I miss the ITR filing deadline?

Q11: What is an updated return (ITR-U) and when can I file it?

Q12: Does Finoda file ITR for NRIs?

Q13: What is the income tax slab for the new tax regime in FY 2025-26?

Q14: How do I check my income tax refund status?

About Finoda's Tax Team

Finoda operates from Bangalore and serves clients across India. Our tax advisory team includes qualified Chartered Accountants who practice under the guidelines of the Institute of Chartered Accountants of India (ICAI). Every return is prepared and reviewed by a licensed professional — not an algorithm.

We operate under SEBI guidelines across our investment and advisory services, and our tax practice follows the Income Tax Act, 1961 in letter and spirit.

Finoda office address: VGV Towers, Unit 101, 139/88, 1st Floor, 100 Feet Ring Rd, Jayanagara 9th Block, Bengaluru – 560041