ELSS Funds India 2026 — Best Tax-Saving Mutual Funds with Highest Returns

Every March, millions of salaried Indians scramble for last-minute 80C tax-saving proofs. Most end up putting money wherever is fastest — not wherever is smartest. In our experience helping thousands of investors across Bangalore and across India, ELSS mutual funds are consistently the most overlooked and the most rewarding option in the entire Section 80C basket. They give you equity-linked growth, a short 3-year lock-in, and a real chance at building wealth — not just saving taxes. This guide walks you through everything you need to know, without the jargon.

Table of Contents

- What is ELSS? Understanding the Basics

- Why ELSS is the Best 80C Tax-Saving Investment

- Best ELSS Funds in India 2026 — Expert-Curated List

- ELSS 3-Year Lock-In — What Actually Happens at Maturity?

- How to Invest in ELSS via SIP for Tax Saving

- ELSS Tax Treatment — LTCG After 3 Years Explained

- Common ELSS Mistakes Investors Make (And How to Avoid Them)

- Frequently Asked Questions (FAQs)

- Why Investors Trust Finoda for ELSS Guidance

- Related Guides from Finoda's Education Hub

What is ELSS? Understanding the Basics

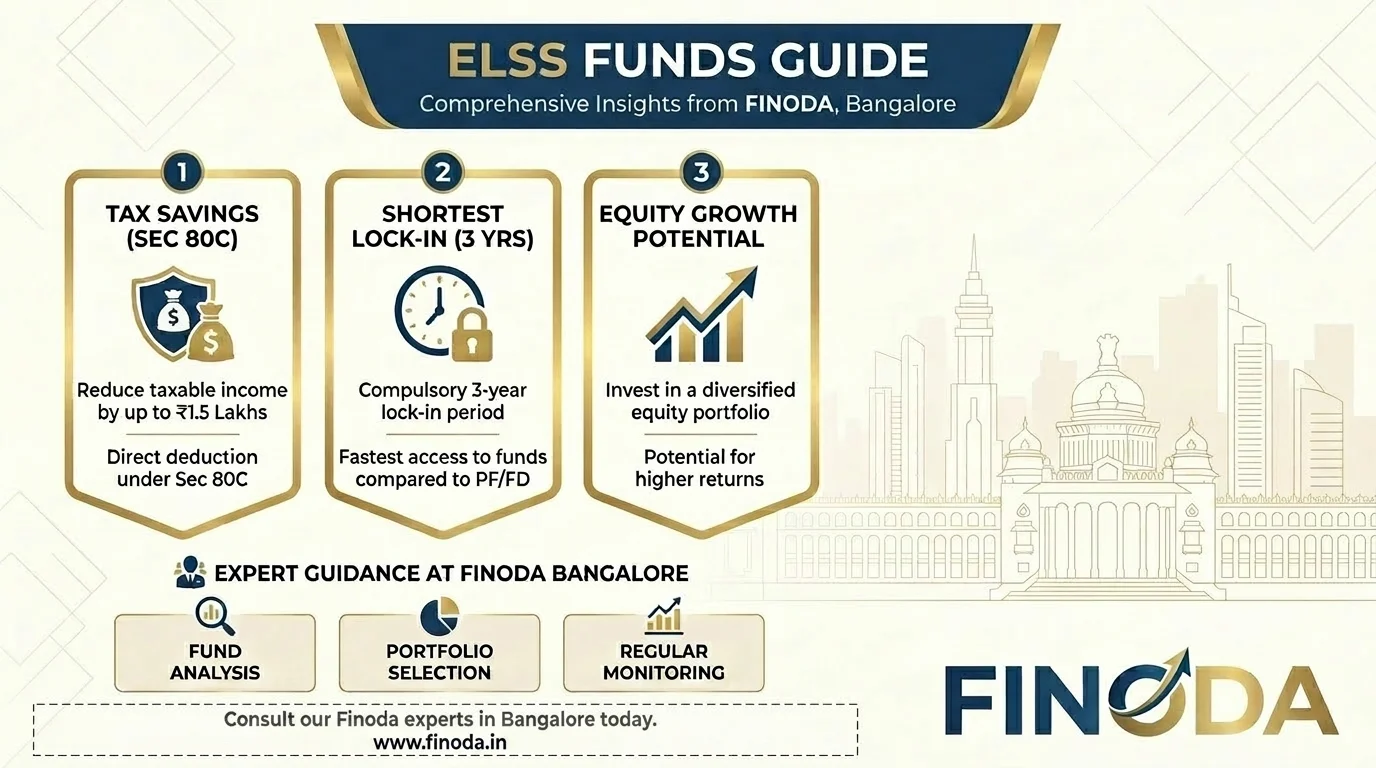

ELSS stands for Equity Linked Savings Scheme. It's a type of diversified equity mutual fund that qualifies for tax deductions under Section 80C of the Income Tax Act.

But here's what makes it different from every other 80C option: ELSS puts the bulk of your money into the stock market. At least 65–80% goes into equities — large-cap companies, mid-cap growers, sometimes small-cap bets. The rest sits in debt instruments. The result? Returns that have historically outpaced every other tax-saving instrument in the 80C universe.

The "savings" part of the name refers to the tax angle. You invest up to ₹1.5 lakh in a financial year and claim a full deduction on that amount under Section 80C. For someone in the 30% tax bracket, that's up to ₹46,800 saved in taxes in a single year.

Who Should Invest in ELSS?

ELSS isn't for everyone, and that's worth saying plainly. If you need your money back in two years, this is not the right place to park it. But if you're a salaried professional, a self-employed individual, or a business owner who pays income tax under the old tax regime — and you're comfortable with a 3 to 5-year investment horizon — ELSS makes a strong case for itself.

First-time equity investors often find ELSS to be a great starting point. The lock-in actually works in your favour — it forces patience, which is the one thing most investors lack.

Why ELSS is the Best 80C Tax-Saving Investment

Let's be direct: ELSS beats PPF, NSC, tax-saver FDs, and most traditional 80C instruments on one key metric — return potential. We've seen this play out repeatedly with clients who moved a portion of their 80C allocation to ELSS five or seven years ago.

Here's the core argument. PPF currently earns 7.1% per annum — guaranteed, but fixed. ELSS, over a 10-year period, has averaged around 12–15% CAGR across most well-managed funds. That difference compounds heavily over time.

Moreover, ELSS has the shortest lock-in of any 80C investment — just 3 years. PPF locks you in for 15 years. NPS locks your money till you're 60. Tax-saver FDs block access for 5 years. With ELSS, you're free to redeem after 3 years — or stay invested if the market is doing well.

ELSS vs PPF vs NPS — Quick Comparison

| Feature | ELSS | PPF | NPS |

|---|---|---|---|

| Lock-in Period | 3 years | 15 years | Till age 60 |

| Returns | Market-linked (12–15% avg.) | Fixed (7.1%) | Market-linked (~10–13%) |

| Tax on Returns | 12.5% LTCG above ₹1.25L | Fully exempt | Partially taxable |

| Min. Investment | ₹500/month (SIP) | ₹500/year | ₹500/month |

| Extra Deduction | No | No | ₹50K under 80CCD(1B) |

| Risk Level | High (equity) | Nil | Low to Medium |

Verdict from our team: For growth-oriented investors with a 5+ year horizon, ELSS delivers the best return potential. But PPF and NPS serve different goals. Many clients at Finoda run all three — ELSS for growth, PPF for stability, NPS for the extra ₹50,000 deduction.

Best ELSS Funds in India 2026 — Expert-Curated List

Not all ELSS funds are created equal. Fund manager quality, expense ratio, portfolio concentration, and consistent performance over 5–10 years — these things matter more than short-term rankings.

In our experience, the following funds have consistently shown strong risk-adjusted returns over the long term. These are funds our team has researched and discussed with clients, and they come up repeatedly in advisor conversations across India.

Funds that have consistently topped the ELSS category (based on 5-year CAGR):

- Quant ELSS Tax Saver Fund — Among the highest 5-year returns in the category (~28–29% CAGR as of 2025), driven by active, high-conviction stock picking. Higher volatility, but for aggressive investors, it's hard to ignore.

- Motilal Oswal ELSS Tax Saver Fund — Delivered 28.76% XIRR over 3 years as of July 2025. Concentrated portfolio with strong stock selection.

- Mirae Asset ELSS Tax Saver Fund — Consistent large-cap-oriented fund. Lower volatility and strong long-term track record. Good choice for moderate-risk investors.

- SBI Long Term Equity Fund — One of India's oldest ELSS funds. Proven over multiple market cycles. Suitable for conservative-to-moderate investors.

- ICICI Prudential ELSS Tax Saver Fund — Blended approach across market caps. Solid 10-year performance.

- DSP ELSS Tax Saver Fund — Good mid-cap exposure, strong 10-year CAGR. Zero exit load post lock-in.

⚠️ Disclaimer: Mutual fund investments are subject to market risks. Past returns do not guarantee future performance. Please consult a qualified financial advisor before investing.

We always recommend looking at both 3-year and 10-year returns — not just whichever number looks good right now. A fund that's been consistent over a decade has survived at least two or three bad market cycles. That matters.

ELSS 3-Year Lock-In — What Actually Happens at Maturity?

The 3-year lock-in is one of the most misunderstood parts of ELSS investing. Let us clarify how it actually works.

When you invest a lump sum in an ELSS fund, that entire amount gets locked in for exactly 3 years from the date of investment. After 3 years, you can redeem freely — or leave it untouched and let it continue growing.

But SIP works differently. Each monthly SIP instalment carries its own 3-year lock-in. So a SIP done on 1 January 2026 can only be redeemed from 1 January 2029. The February 2026 instalment is available from February 2029, and so on. This means if you've been doing a 12-month SIP and you want to redeem everything at once, you'll need to wait until the last instalment completes its 3-year window.

This is actually a planning point many people miss. If you plan to stop and withdraw, pause your SIPs 3 years before you need the money. Otherwise, the most recent instalments will still be under lock-in.

What Should You Do After the Lock-In Ends?

Honestly? In our experience, most investors are better off staying put. The 3-year lock-in is just the minimum. Equity mutual funds generally do their best work between 5–10 years. Many investors who've stayed invested for 7–10 years have seen their ELSS corpus multiply several times over.

If you need the money for a goal — a house down payment, your child's education — redeem what you need. Otherwise, there's no harm in treating ELSS as a long-term wealth creation vehicle, not just a tax-saving tool.

How to Invest in ELSS via SIP for Tax Saving

SIP — Systematic Investment Plan — is the cleanest way to invest in ELSS for most salaried investors. Instead of scrambling in February or March to invest a lump sum, you invest a fixed amount every month, automatically.

Here's the practical approach we recommend to clients:

- Start with a target. If you want to use ELSS for your full ₹1.5 lakh 80C deduction, you need about ₹12,500 per month in SIP.

- Pick 1–2 funds. Don't spread across five ELSS schemes. The diversification is already built into the fund itself.

- Set up auto-debit. Most platforms let you automate this from your bank account on a fixed date.

- Don't stop during market dips. SIP works through rupee cost averaging. A dip just means you buy more units at a lower price.

- Review annually. Check performance against the benchmark, not other random funds. If the fund is consistently underperforming its benchmark for 3+ years, consider switching.

You can start ELSS SIPs with as little as ₹500 per month. There's no upper limit on investment — though the tax deduction caps at ₹1.5 lakh under Section 80C.

Also read SIP vs Lumpsum — Which is Better?

ELSS Tax Treatment — LTCG After 3 Years Explained

Here's the tax part, explained simply.

When you redeem your ELSS units after the 3-year lock-in, the gains are treated as Long-Term Capital Gains (LTCG). As of the current tax rules (FY 2025–26):

- Gains up to ₹1.25 lakh per financial year are completely tax-free.

- Gains above ₹1.25 lakh are taxed at 12.5% LTCG (without indexation benefit).

So if you redeem ₹2 lakh in profit in a year, only ₹75,000 (above the ₹1.25L exemption) will be taxed at 12.5%. That works out to a tax of about ₹9,375 — which is quite reasonable on a significant gain.

There's no short-term capital gains tax on ELSS, simply because you cannot redeem before 3 years anyway. The lock-in effectively enforces long-term tax treatment.

Important: The 80C tax deduction is available only under the old tax regime. Under the new tax regime, Section 80C deductions are not applicable. If you've switched to the new regime, ELSS may still make sense as a long-term equity investment — but not purely for the tax deduction.

Visit Tax Advisory Hub for complete tax planning guidance

Common ELSS Mistakes Investors Make (And How to Avoid Them)

We've guided thousands of investors, and the same mistakes come up again and again. So let's call them out.

Mistake 1 — Investing in March every year in a rush. Last-minute lump sum investing increases timing risk. A SIP spread across the year is smarter and far less stressful.

Mistake 2 — Choosing based on last year's returns. Last year's top ELSS fund is often this year's laggard. Look at 5 and 10-year consistency, not one-year charts.

Mistake 3 — Redeeming as soon as the lock-in ends. Three years is often not enough for equity to fully deliver. Many investors who stay 5–7 years see dramatically better outcomes.

Mistake 4 — Investing only in ELSS and nothing else. ELSS is good, but a balanced portfolio also needs debt, insurance, and emergency liquidity. ELSS should be one part of a larger plan.

Mistake 5 — Not considering the new vs old tax regime before investing. If you're on the new regime, the 80C deduction isn't available. Make sure you know which regime you're filing under before committing.

Frequently Asked Questions (FAQs)

1. What is ELSS and how does it work?

ELSS (Equity Linked Savings Scheme) is a type of mutual fund that invests primarily in stocks and qualifies for tax deductions under Section 80C of the Income Tax Act. You invest money, the fund manager allocates it across equities, and after a mandatory 3-year lock-in, you can redeem. Returns are market-linked, not guaranteed.

2. How much tax can I save through ELSS?

You can invest up to ₹1.5 lakh in a financial year and claim a full deduction under Section 80C. For someone in the 30% tax bracket, that saves up to ₹46,800 in taxes annually (including 4% education cess). This deduction is available only under the old tax regime.

3. Is ELSS better than PPF?

For investors with a moderate to high risk appetite and a 5+ year horizon, ELSS typically delivers better returns than PPF. PPF currently offers 7.1% fixed returns, while well-chosen ELSS funds have averaged 12–15% CAGR over 10 years. However, PPF is safer and fully tax-exempt at maturity. They serve different goals — many investors use both.

4. What is the minimum amount to invest in ELSS?

You can start an ELSS SIP with as little as ₹500 per month. For lump sum, most fund houses accept a minimum of ₹500 to ₹1,000. There's no upper limit on investment, though the tax benefit under 80C is capped at ₹1.5 lakh per year.

5. Can I withdraw ELSS before 3 years?

No. ELSS has a mandatory 3-year lock-in from the date of each investment. You cannot redeem or switch units before that period, even in a financial emergency. This is why you should only invest money you won't need in the short term.

6. How is ELSS taxed on redemption?

Gains after the 3-year lock-in are treated as Long-Term Capital Gains (LTCG). Gains up to ₹1.25 lakh per year are tax-free. Gains above ₹1.25 lakh are taxed at 12.5% without indexation benefit (as per FY 2025–26 rules).

7. Is ELSS available under the new tax regime?

The Section 80C deduction for ELSS is not available under the new tax regime. However, you can still invest in ELSS as an equity mutual fund for wealth creation — you just won't get the tax deduction. Confirm which tax regime you're filing under before investing for 80C benefits.

8. How does SIP work in ELSS?

Each SIP instalment in ELSS has its own 3-year lock-in from the date that instalment was invested. So a SIP done in January 2026 can be redeemed from January 2029, and a SIP done in February 2026 can be redeemed from February 2029. You cannot redeem all instalments at once unless all of them have completed 3 years.

9. Which is the best ELSS fund in 2026?

There's no single "best" fund — it depends on your risk appetite and investment horizon. As of 2026, funds like Quant ELSS Tax Saver, Motilal Oswal ELSS Tax Saver, Mirae Asset ELSS, and SBI Long Term Equity Fund have performed strongly. We recommend comparing 5-year and 10-year CAGR, expense ratio, and benchmark consistency before choosing.

10. Can I invest in more than one ELSS fund?

Yes, absolutely. There's no restriction on investing in multiple ELSS funds in a financial year. However, the combined 80C deduction is still capped at ₹1.5 lakh across all investments. From a diversification standpoint, 1–2 good ELSS funds is usually enough, since each fund is already diversified internally.

11. Is ELSS safe for first-time investors?

ELSS invests in equities, so it carries market risk — your investment value can go up or down in the short term. However, for first-time investors with a 5–7 year horizon, ELSS is a reasonable entry point into equity markets. The lock-in enforces patience, which often leads to better outcomes than freely redeemable funds.

12. Can I do ELSS through SIP and claim 80C deduction?

Yes. SIP investments in ELSS are fully eligible for Section 80C deduction, up to ₹1.5 lakh in a financial year. Each monthly SIP instalment counts towards your annual 80C limit. So a ₹12,500/month SIP across 12 months = ₹1.5 lakh deduction for that financial year.

13. What happens to ELSS after the 3-year lock-in?

After 3 years, your ELSS units become freely redeemable. You can redeem all, redeem partially, or continue holding. The fund doesn't automatically close — it simply converts to an open-ended fund for your units. Many investors continue holding for better long-term compounding.

14. Is ELSS a good option for retirement planning?

ELSS is a good wealth creation vehicle, but it's not designed specifically for retirement. For retirement, NPS or a combination of equity mutual funds and PPF typically works better. That said, ELSS can be one component of a retirement corpus, especially for investors in their 30s and 40s with a 15–20 year investment horizon.

Why Investors Trust Finoda for ELSS Guidance

We're a Bangalore-based investment advisory team. Our operations follow the guidelines set by SEBI — the Securities and Exchange Board of India — the apex regulatory body for India's capital markets. We've worked with over 10,000 investors across trading, mutual funds, insurance, and tax planning. More importantly, we've built a culture where advisors are trained to recommend what's right for the client, not just what's easy to sell.

With ELSS, our approach is straightforward. We look at your age, income, tax bracket, investment horizon, and risk comfort — and then we help you choose the right fund, set up the right SIP, and understand what to expect. No pressure, no jargon.